The Pantiles, Royal Tunbridge Wells – photo Paul Collins

Media commentary on British prime minister Rishi Sunak’s cabinet reshuffle largely misses the point – the exception being the FT’s Stephen Bush, whose newsletter came out after I started drafting this – and who is absolutely on point here. Most reflect on the ironies of the shock appointment ex-prime minister David Cameron to be Foreign Secretary, and the impact this may have on various groups of voters. Many cast it as the desperate act of a failing administration. I would rather see it as a rather brilliant move to the front foot.

First things first. The most important move yesterday was the removal of Suella Braverman as Home Secretary. She was never qualified for the job and, predictably, proved a loose cannon. But she is a darling of the Tory populist wing, who gave her a rapturous reception at the party conference – and her appointment was widely regarded as necessary for Mr Sunak to secure his uncontested nomination to the top job. Last week her attention-seeking criticism of the pro-Palestinian demonstrations and criticism of the police helped take the heat off Labour leader Sir Keir Starmer’s typically leaden response the Gaza crisis. This was an excellent opportunity for the Conservatives to cast doubt on Sir Keir’s ability to take on the job of prime minister. Instead the story was Ms Braverman’s extraordinary conduct – which included direct defiance of Mr Sunak in an article published in The Times. That undermined Mr Sunak’s authority. This exasperated respectable Tory-leaning voters in places like Tunbridge Wells, without doing much to rally disaffected voters in places like the West Midlands, site of a recent spectacular by election loss, which had been critical to the party’s success in 2019.

But by appointing Lord Cameron, as we must now call him, to the cabinet Mr Sunak relegated the Braverman story to the back pages. Instead of outrage by her supporters bringing attention to the fractured state of the Conservative Party, all anybody wanted to talk about was Lord Cameron and Mr Sunak stamping his mark on on the cabinet. Ms Braverman’s sacking was passed off with a shrug as a rather obvious move. She will try to regain the initiative – she is clearly politically ambitious – but it will be hard for her to recover. Her moment has passed. The Tory populists will seek out other standard bearers.

This will do much to reassure those voters of Tunbridge Wells, a short drive from where I live. Here a traditionally safe Tory seat is under attack from the energetic Lib Dem candidate, Mike Martin. These voters, to generalise, never rejected the Cameron brand of politics, as the West Midlands voters had. To them the problem with Ms Braverman wasn’t really her politics, it was the fact that she wasn’t a team player, and showed no particular signs of administrative competency. To people who are professionals themselves, as so many of these voters are, this is a cardinal sin. It is a point that the Brexit-supporting populists simply cannot understand. The professionals have warmed to Mr Sunak, who is well to the right of their normal politics, because he displays this professionalism – unlike his two immediate predecessors – Liz Truss and Boris Johnson. They abhorred former Labour leader Jeremy Corbyn with a passion, as he was the diametrical opposite of professional.

But, alas for Mr Sunak, Sir Keir is a consummate professional too. As is Sir Ed Davey, the Lib Dem leader – and indeed this group of voters rather liked the Lib Dem – Conservative coalition that Lord Cameron led, and probably like the idea of a Lib Dem-Labour one (anathema as that is to Sir Keir). Mr Sunak may have stopped a rout, but he will need to do more to secure a win.

To do that Mr Sunak will need to show that he is getting to grips with the crisis in public services, and the chaotic illegal immigration in small boats across the Channel. Pretty much all public services are in a sorry state, but the most important politically for now are the NHS, the courts and water and sewage (where problems are close to home in Tunbridge Wells). But to seize the initiative here Mr Sunak will need to unlock public spending, to invest in facilities and to restore lagging pay – otherwise he will not be seen as serious. This matters more than the tax cuts beloved of the Tory right. There is talk of cutting Inheritance Tax, as this is a wedge issue with Labour. Inheritance Tax does weigh heavily in the minds of the wealthier people of Tunbridge Wells, with its high property prices – but my guess is these voters would be unimpressed with such shameless politicking. The forthcoming Autumn Statement from the Chancellor of the Exchequer will be a critical test for this government.

But as Stephen Bush says, just as Mr Sunak was unable to capitalise on gestures to the populists because of his lack of follow-through, he will not capitalise on his gesture to voters of Tunbridge Wells for the same reason.

Recognition of Sir Keir Starmer’s achievement as Labour leader has been grudging. Even as Labour dominates the opinion polls with leads of over 10%, and local elections and by elections confirm it, the response has been “Yes, but…”. Any straw in the wind that might throw doubt on Labour’s dominance is leapt on and magnified. Labour’s victory in two by elections last week, in two ultra-safe Conservative seats, should end that, following as these do a spectacular victory over the SNP in Scotland in a another by election. The party can win almost anywhere it chooses to fight.

The three October by elections each throw a different light on the stranglehold Sir Keir now has on British politics. The first, in Rutherglen and Hamilton West, on the outskirts of Glasgow, shows that Labour is at last breaking the SNP stranglehold north of the border, which resulted in Labour winning just one seat in Scotland the 2019 general election. The constituency was marginal but the swing was huge. This follows the implosion of both the SNP and the Conservatives, which had been the second party in Scotland. This is important, as Labour failure here under both Ed Miliband and Jeremy Corbyn was a critical aspect of the failure of both of these leaders. This makes winning an overall majority in the country as a whole much easier, both directly and indirectly, as the prospect of the SNP holding the balance of power has been used to scare English voters into voting Conservative.

The second by election was in Tamworth, in the West Midlands. This seat shared characteristics with the “red wall” seats that used to be Labour, but which have been swinging to the Conservatives since 2010, and especially in 2019 – and which voted heavily for Brexit. In this case the Conservatives first won it in 2010 and improved their margin in each of the elections in 2015, 2017 and 2019 (even in 2017 when the national swing was against them). Labour’s success here is a sign that Labour is at last reversing this trend; even if it can’t back to 2010 in a general election, pre-2019 will bring in plenty of seats.

The third seat was Mid-Bedfordshire which is altogether more middle-class, and a classic, largely-rural safe Conservative seat that they have always held. What was particularly interesting this time was that the Liberal Democrats fancied their chances here, after their four spectacular by election victories this parliament, including two from third behind Labour, as in this seat. The argument was that many voters might contemplate voting Lib Dem but would never consider Labour. The Lib Dems put in a massive effort on the ground. But Labour’s success in the safe Tory seat of Selby suggested to them that they could win here, putting the Lib Dems in their place. And so it proved. Apart from the battle with the Tories, this was a trial of strength against the vaunted Lib Dem by election machine. Labour won.

Labour can’t win just by reinstating their red wall losses, even back to 2010, or recovering the seats lost in Scotland in 2015 – they lost in 2010 after all. But progress in Mid-Bedforshire and Selby show that they are making ground everywhere except, perhaps, in a few areas where the Lib Dems are already well-established, and London which they already dominate. By contrast their failure in Uxbridge, on the same day as Selby, and which the Conservatives and their supporting commentariat took to be a sign of hope, is an outlier. It is a London seat and London is the one area where the party had progressed since 2010.

All this brings to mind the build-up to the 1997 general election, and Mr Blair’s landslide victory for Labour, when Labour was similarly winning across a broad front. Then too, the Conservatives clutched at every available straw; they talked of creating “clear blue water” between themselves and Labour, much as they do now, without using those words. The Conservative prime minister was John Major, and his advisers kept saying that “the darkest hour is just before the dawn,” oblivious to actual cycle of light (the darkest hour is midnight). Meanwhile Labour shadowed Conservative fiscal plans in order to head off fears about extra taxes – and generally tempered its radicalism. I recently heard a claim that Labour promoted radical policies before 1997, and so should not fear doing so again. This is nonsense: any radicalism was confined to constitutional policies that were popular amongst key minorities, and few others cared much about. There were no promises on country-wide electoral reform or English devolution, and radical increases in spending on the NHS, for example, did not come until Labour’s next term.

But there are differences between now and 1996, and they are interesting. Then Mr Blair was putting most of his energy into winning over liberals. He had an unwritten pact with the Lib Dem leader Paddy Ashdown, but it was a scary time to be a Lib Dem – what was the point when Labour seemed so interested in liberal ideas – promoting education, Scottish devolution, freedom of information – and even some signs of flexibility on electoral reform? Sir Keir is not interested in any of this – except with the adoption of a green agenda, though he is hedging even on that. The Tories have alienated liberals so thoroughly that he doesn’t have to try to win them over. Instead, he is focusing on Brexit-supporting working class and lower middle-class voters, which Mr Blair did not completely neglect (his law-and-order policies were designed to appeal to them), but treated secondary. Sir Keir dead-bats the endless culture war provocations that the Tories throw at him and drives home his message on chaotic state of public services, important to this group. Sir Keir’s uncharismatic style seems calculated to reassure, compared to Mr Blair’s slippery charisma.

Of course, Labour’s strength largely reflects the Conservatives’ weakness. And yet there is little they can do to correct that. Their attempts to imitate the US Republicans with nativist and culturally conservative causes, and rowing back on green policies, seem to have little traction with their key audience, while alienating middle-class liberals, who have been a key part of their electoral coalition. Perhaps their best hope is to stoke up fears of tax rises under a Labour government. But the dire state of public services has probably reconciled most people to higher taxes, and the Conservatives have shredded their reputation for competent management. Even those who think the prime minister Rishi Sunak is competent, will not think the same of most of his colleagues, and will have noted how often the party ditches its leaders.

Big swings can happen in a short space of time. A notable case was in 2017 when Theresa May lost a commanding lead over Labour in weeks. But that was a snap election when neither side was prepared, and Mrs May compounded it by trying to capitalise on her lead by putting risky policies in the party manifesto. Most people expect the Conservatives to close the gap a little, leaving Labour with a small majority or just short. But a complete Tory meltdown is also on the cards, such is the party’s weak credibility and penchant for self-destruction.

There are legitimate questions over Sir Keir’s policies. His talk of making public services work better through reform, and not by radically increasing funding, is just not credible. Furthermore, the public finances are looking weak. High inflation means a tight monetary policy. The country still depends on funding from foreigners, and yet the funding environment is getting much more difficult. Promising to fill this gap by growing the economy lacks credibility too, given the headwinds of demography, the retreat on open trade, and the rise of low-productivity services.

But whatever the doubts, Sir Keir Starmer is offering a much more convincing alternative government to the Conservatives, and there seems to be nothing the latter can do about it.

Bournemouth – site of the 2023 Lib Dem Autumn Conference

I haven’t posted for a month. I’ve been on holiday, and then last weekend I went to the Liberal Democrats conference in Bournemouth. This is the first in-person Autumn conference the party has had this parliament, since September 2019 in fact – and my first conference of any kind since then. It was lovely to catch up with friends and acquaintances, people-watch and sample some of the internal debates the party is having. But what did the event say about the health of the party?

Overall the party was in good heart after a series of spectacular by election wins and good local election results. This was widely expected to be the last Autumn conference before the next general election (a shorter Spring conference in March in York should go ahead) – which is expected next year in May or in September or October. It showed. Much passion was on display on the conference floor, and many excellent speeches – but little actual debate: few speaker’s cards were placed against motions or even amendments. It resembled the managed affairs of the Labour and Conservative parties. There was one notable exception, on housing, which I will come to.

The party leadership’s electoral strategy is clear: it is to increase the party’s representation in parliament to thirty or more seats (it is now 11 plus four by-election wins), almost entirely by winning seats currently held by the Conservatives (one or two SNP seats are in the sights, and perhaps the odd Labour one). The unspoken hope is that this will be enough to overtake the SNP as the third party in parliament, with a substantial increase in the party’s ability to influence the agenda there. It may also be enough to hold the balance of power, should Labour fail to secure a majority, and thus influence government policy in one way or another.

The contrast with 2019 could hardly be greater. The party then had momentum as a rallying point for those hoping to reverse the result of the Brexit referendum – and it talked of forming the largest party in parliament with its leader as prime minister. A lot of political capital was spent on the proposition that the party would not rerun the referendum if it won an overall majority. But the party was out-manoeuvred by Labour’s support for a second referendum (much good that it did them) and the bubble was burst in the December 2019. Following this debacle the party commissioned a post-election review by Baroness Thornhill, who, as mayor of Watford, was one of the party’s most successful politicians. Unlike most such reviews, which are generally discarded by the party managers before the next election arrives, this review has been taken to heart. Ambition has been lowered; the communications agenda is led by public opinion rather than activists’ priorities; efforts have been made to professionalise the party’s core workers and reduce staff turnover.

This gives a great deal of credibility to the party’s strategy. Early in the conference many activists were a bit glum after seeing a presentation by psephologist John Curtice that showed that the collapse in support for the Conservatives was benefiting Labour and not the Lib Dems. But what matters is what is happening in about fifty seats out of the 650, and national polls will not show this clearly. Another pollster, Rob Ford, showed that the party was doing well among better-off graduate voters, and that the numbers of these voters was increasing in the seats likely to be Lib Dem targets. The Tories’ courting of “petty bourgeois” voters by ditching green policies, and ratcheting up nasty rhetoric on immigrants, plays into Lib Dem hands here. In 2019, the Tory leader Boris Johnson was careful to nod to these voters; the current leadership knows no such subtlety. The Lib Dems should benefit from the collateral damage of the Labour-Tory contest for the petty bourgeois – rather as the Tories benefited from the collateral damage of the Labour-Lib Dem battle for the professional classes in 2019. The party’s prospects thus look good in a decent number of seats in the South-East commuter belt around London, and equivalent seats further north, such as Hazel Grove outside Manchester. The prospects are murkier in the party’s former heartlands in the west county, however, where the professional classes are much less in evidence – though with Labour relatively weak there, there must be some opportunities.

However this strategy is creating a lot of tension in the party. Listening to the electors and letting them set the agenda may be good for curbing arrogance and winning parliamentary seats, but party activists want something more ideological and radical. But the radicalism is being suppressed. The party will not explicitly campaign to rejoin the European Union, as many activists wish – a goodly proportion having joined the party in the first place because of support for EU membership. Rather like Labour, the leadership are sticking to a much vaguer line about better relations. A flirtation with Universal Basic Income (UBI) has been firmly squashed – though in general the party remains stronger on ideas for spending more public money that raising it or saving it. This conservatism led to the only serious, open conflict of the conference: on housing.

Housing developments are not generally popular in the rural and semi-rural areas that comprise the party’s best prospects. City-dwellers fume that this is “nimbyism”, but living in one such area (bordering decent Lib Dem prospect seats, though not actually in one) I can say that this is oversimplifying things bit. Many developments comprise mediocre-quality houses in environmentally sensitive areas, with inadequate plans for supporting infrastructure – because these are more profitable for developers. The Conservatives are in full retreat on their commitment to building more homes, and are attacking the Lib Dem national target of building over 300,000 houses a year (even if this commitment was in their 2019 manifesto too) – though this did not do the Tories any good in local elections here in Sussex. The Lib Dem leadership were worried enough about this to propose dropping this target in a new housing policy, while at the same time still committing to building roughly this number of homes, by increasing social housing, developing garden cities, and so on. But the Young Liberals organised a counter-attack. Younger voters feel as if they are the centre of a housing crisis, with increased rents and vanishing prospects of buying their own homes. The housing target has important symbolic value to them, and the policy looked like a retreat. The leadership tried to win by deploying heavyweight speakers, but their arguments were thin gruel. Former leader Tim Farron delivered a “barnstorming” speech in defence of the leadership position by shouting increasingly loudly that housing targets wee “Thatcherism” without explaining why. “Has he lost the plot?” my wife, next to me, asked. “Yes,” I said, and we both voted for the Young Liberal amendment, which was carried. That was the only act of defiance by the membership, however.

In the conference fringe, things were a lot more interesting. My especial interest was rural policy: how to turn around farming policy so that it helps restore wildlife and absorb carbon – without too much damage to productivity. For me this is a critical area: carbon policy will fail unless the land is made into an efficient carbon sink, and we end extractive farming practices – never mind ending the destruction of wildlife. I was encouraged by the party’s support for this, which is winning converts among many farmers. But hard choices beckon, as it is hard to see how this can work without a substantial reduction in the consumption of meat. I was also interested by the arguments made in favour of UBI at a couple of fringes. There is something deeply flawed in the conventional thinking about tax, benefits and public services – and UBI might be part of the solution. But if it is, it feels like only one leg of a three-legged stool and it will not work by itself. More on that on this blog later, as I gather my thoughts.

In his closing speech, the party leader, Ed Davey, harped on the familiar themes: outrage at water companies for dumping sewage into rivers and the sea, supporting Net Zero policies, and a new policy about health care and cancer treatment. What party activists were more interested in were his mentions of closer relations with Europe, advocacy of electoral and political reform and an attack on Labour for lacking ambition and caving in to Tory policies. He said about the minimum here, in comments that were not picked up by the media coverage. The attitude to Labour is interesting. There is no love lost between Labour and the Lib Dems. The two parties are battling against each other to win the Conservative held seat of Mid Bedfordshire in a by-election, in an interesting trial of strength. Activists were repeatedly called on the help there. The party needs Labour voters to come over to it in its key seats, and so is careful not to antagonise.

I think Ed is right in his overall approach. The next election will clear a lot of air, and hopefully the party can develop its more radical instincts afterwards. If Labour win, as seems likely, then the party will need to define itself clearly against it – and that will be a lot more interesting.

Oh dear! The New Statesman magazine is returning from its summer break with what it obviously hopes to be a major piece by Harry Lambert, its editor, to challenge Labour Party policy. Mr Lambert shows his credentials as a journalist with extensive reportage. But there is nothing here that anybody who wants to seriously understand tax and the economy to get their teeth into – it is the intellectual equivalent of ultra-processed food. Your taste buds might be excited but it is not nutritious fare. To be fair, it’s not immediately apparent that either the Labour leader, Sir Keir Starmer, or the Shadow Chancellor, Rachel Reeves, are seriously interested in economics – and these are the people the article sees to influence. But the pair are very much interested in hard politics, and the article fares no better in that department.

The article reinforces my suspicion of anything in a journal billed as a “long read”. I’ve noticed a propensity to do this both in The Guardian and the Financial Times. I take this as a warning to stay clear, to avoid articles that aren’t properly edited and waste a lot of reading time*. Mr Lambert’s article was not billed as a long read, but it should have been – there is a mass of verbiage, which you have to wade through before you come to his three policy proposals, and even these aren’t stated succinctly. These proposals are: to replace Council Tax with a 0.5% tax on property values (covering just domestic property, as far as I can see); applying National Insurance to property rental income; and raising the rate of Capital Gains Tax. These, he estimates would raise £28 billion a year (though the property tax reform would be revenue-neutral): not coincidentally the amount of Labour’s proposal for spending on the green energy transition, which they are now backtracking from. More sensibly he suggests that the extra revenue is used to reduce tax on work (income tax, or better still, National Insurance).

I will start by reflecting on the overview, which is summarised by this statement:

In order to spend money in government the party will need to raise it. There is a very good way to do that. It is to shift the tax burden away from labour and on to capital, away from work and on to wealth.

Harry Lambert, New Statesman 30 August 2023

There are two words of warning on this. The first is that the words “wealth” and “capital” are treated as synonyms (as are “labour” and “work” more justifiably). They can be, but when talking about economics they are different things. Capital refers to the assets tied up by businesses in order to be able to operate: premises, machinery, working capital and so on. By and large it isn’t a good idea to tax this directly, as it would reduce investment. Taxes on profits generated by the capital before it is distributed to owners – such as corporation tax – is another matter. This is in effect a tax on capital, but a very efficient one. It is one of the few things that the Prime Minister and Chancellor Rishi Sunak has insisted on raising, in contrast to his predecessor as Chancellor, George Osborne. Wealth, on the other hand, is owned by individuals for their disposal. The proposed property tax is a tax on wealth, not capital, unless it is applied to businesses too. That applies to Capital Gains Tax too (demonstrating that the word “capital” has yet another nuance when applied to taxes). Where the proposed extra tax on property rent sits is ambiguous.

The second word of caution comes from Modern Monetary Theory (MMT). This way of looking at things seems to be currently out of fashion, but I think that it captures many economic realties quite well. Supporters of MMT suggest that the main purpose of taxes is to manage demand in the economy, to prevent excess demand leading to inflation. It isn’t to manage the national debt, which can be paid off by creating money – if that is under national control, as it is in the UK. MMT was popular on the left once because it was suggested that the country could expand public spending without raising taxes, because inflation was dormant. Alas the excess spending across the Covid pandemic has led to inflation, showing that the inflation constraint is a real one, even if the national debt wasn’t – though to be fair that is also because the pandemic and other factors, such as the Ukraine war, constrained supply. The problem is that taxes on “work” (or spending, such as Value Added Tax) are much more effective at this demand management job than are taxes on wealth, as the wealthy spend a much lower proportion of their assets on consumption. So taxing more on wealth to tax less on incomes is in practice a much trickier exercise than it might first appear. Which is not to say that there aren’t good reasons to tax wealth, of course. It is good for managing the national debt (which is harder some supporters of MMT appear to think) , but much less so for funding increases in public spending.

But the main problem with Mr Lambert’s proposals is that they clearly haven’t been thought through. The country is surely sick of half-baked policies that turn out to be nightmares (Brexit, NHS reform – don’t even mention Liz Truss). The new property tax and the tax on rental income are radical changes which raise a lot of important questions of detail. Council Tax may be awful, but it contains a warning. There has not been a revaluation of the tax since it was introduced 30 years ago because of the political and logistical difficulties. How are property valuations to be determined and maintained? Then there are other questions: how would business assets be treated? Wouldn’t it be better to tax land values instead (there is a long history of advocacy of Land Value Tax)? And tax on rental income? What about properties owned by companies? And what would be the impact on rents and the availability of property to let? Mr Lambert can point to no major piece of research that tackles the details.

The fuzziness of such details would make the policies very easy to attack should Labour try to adopt them – and in fact they would take years to design and implement. The best way for the Labour leadership to take them forward is to propose them after they take power, as part of a comprehensive review of taxes to make the system fairer, and use the full resources of government to design them – and then put them to the country in the election after next. Meanwhile they wouldn’t need to even put the idea into their manifesto. Raising tax on capital gains is another matter – this has gone up and down periodically, and could be done relatively easily. And it would be not at all surprising if Labour did this in government. But there’s no need to highlight it now.

Which brings us to the high politics. Alas opinion polling on subjects like this that are not a matter of intense national debate are nearly useless. I can draw a parallel with electoral reform. In polls most people supported the idea: until a referendum in 2011 made it politically contested, when it was crushed. The political problems is as ever, is what people are now starting to once again call the petty bourgeoisie (or petit bourgeoisie if you prefer). These are self-employed people, or others who aren’t tied to major businesses or government agencies, who have the idea that they have made their own way in life with little help from government. They are electorally decisive but sceptical of big government and taxes of any sort. The political right are absolute masters of presenting taxes on the very wealthy as attacks on this group. This is why the Labour leadership are treading so carefully on tax. They think they are going far enough already by proposing changes to the taxation of private schools and non-domiciled taxpayers.

Harry Lambert’s ideas just aren’t ready to present to the electorate. That is the reason that the Labour leadership will ignore them – and wait until they have the resources of government to develop them.

*Readers might consider this cheeky as my own articles aren’t short by journalistic standards – but I don’t like things very short either!

Last weekend The Observer reported that a senior Conservative had suggested that the Tories were in danger of being the “nasty party” again. They needed to show more humanity, he said. This followed some provocative language on the subject of asylum seekers from the Home Secretary and the party’s deputy chairman. The nasty party epithet resonates because it was attributed to the party during the long period of its doldrums while Tony Blair was prime minister, and and the party suffered three crushing defeats to Labour in general elections. It took a conscious rebranding effort by David Cameron to break free of the tainted Tory brand.

The Tory brand is undoubtedly deeply tainted once more. Their poll ratings are dire. Even in traditional heartlands, like where I live in rural Sussex, the party is being rejected in local elections by spectacular margins. Nice middle class people treat the party with disdain. The party’s main electoral strategy, though, is not to woo these voters but lower middle class and older working class voters who were part of the anti-establishment coalition that supported Brexit, and flocked to the party in 2019 in the “Get Brexit Done” election. It now seems that appealing to these voters is one of the driving principles of government policy, casting aside all considerations of national or wider interest. These voters are thought to like the “nasty party” image.

The problem of small boat crossings across the Channel illustrates the government predicament well. It is this flow of illegal immigrants that provoked those nasty comments. The government promotes a series of “tough” but token policies – such as trying to transport migrants to Rwanda, and housing them on a barge that looks distinctly like a prison ship. Ministers then attack “leftie lawyers” for slowing down (or even stymieing) these ideas, in the hope that mud will stick to Labour, led by lawyer Sir Keir Starmer. Certainly the flow of migrants across the Channel irritates Brexit-supporting voters, who are no sticklers for the rule of law.

But the flow of boats goes on. There is apparently a slight dip in numbers in 2023 compared to 2022, but this may just reflect weather conditions. The people traffickers are getting better organised, and are easily able to outwit government efforts to impede them. For some rather puzzling reason government ministers have been claiming that their policies are designed to “break the business model” of the traffickers. Perhaps they think this form of words sounds clever. But their policies are not directed at this goal at all. The business model depends on the absence of legal routes of migration, or even alternative illegal means – this forces migrants into the traffickers’ arms, allowing them to extract high prices and therefore invest significant money and effort in beating the government efforts efforts to make their lives difficult. Of course the government does not feel it can offer alternative routes, because that means letting more in legally, and their whole aim is to reduce flows overall.

And the longer the flows persist, the more the government has to confront difficult questions. The first of these is why all this is blowing up now, after Brexit, when Brexit was meant to enable Britain to “control its borders”. The business of managing borders is clearly a lot harder than most Brexit advocates had said. Then there is the the rather pathetic scale of the Rwanda and barge policies compared to the volume of incoming people: hundreds compared to tens of thousands. Worst of all is the effect of painfully slow processing of asylum claims, which has left tens of thousands in limbo, many having to be put up at state expense. What the government has not quite admitted was that this backlog arises from deliberate incompetence, as the former Home Secretary Priti Patel seems to have though that processing claims more slowly would reduce the incentives for people to come over and make claims. That hasn’t worked: instead state agencies and their political masters are made to look chronically ineffective.

Polls now show that few people think that the government will fail to stem the flow of boats. In the short term it might work for the Conservatives to deflect the anger towards the liberal “elites”, personified by leftie lawyers. But we probably have more than a year to wait before the next election. It is hardly worth suggesting that the opposition would do no better, when it doesn’t look as if things could get much worse.

If it is to turn the tide of opinion, the Conservatives needs to demonstrate competence above all else. Those nice middle class voters will forgive a lot of nastiness for that. Angry Brexiteers are not so dissimilar. And as for international standing, foreigners have their nasty side too – it is competence that inspires their respect. The problem for the party is that it has turned incompetence into something of a feature since they chose Boris Johnson as their leader. Both he and his successor, Liz Truss, openly selected cabinet ministers on the basis of loyalty rather than ability. Political posturing mattered above all.

Since then there have been an endless succession of ministers evidently not up to the job. Mr Sunak seemed to break from that idea. His stock (and the government’s) was never higher than when he reached a deal with the European Union over Northern Ireland – allowing competence to trump political posturing. But then again, his appointment of the inexperienced but ideological Suella Braverman as Home Secretary always pointed in a different way. Now political messaging is once again the priority, as the government stumbles from one mishap to another.

This recalls the government of John Major in the 1990s, with the party exhausted and fractious after the Thatcher years. It is true that this government managed to pull off an election win against the odds in 1992 – but at that point the government was being given the benefit of the doubt on its economic strategy, while doubts over Labour leader Neil Kinnock persisted. By 1997 the government’s haplessness was exposed to all, while his Labour opponent, Tony Blair, was the very picture of slick competence. Sir Keir can’t aspire to Mr Blair’s heights, but he looks competent enough. Mr Sunak’s supporters may keep clutching at straws (as did Mr Major’s “the darkest hour is just before the dawn”, they said, inaccurately) but it is heading for humiliation all the same.

I apologise for not posting for some time. Feelings of futility and despair at politics have made gardening and painting model soldiers a more attractive pastime. I started an article last week, but this collapsed in a muddle. This time I want to step back and set current debates over the political economy in the broader historical context – to suggest that we need to adjust our expectations to profound changes to the way economies work. Above all this means letting go of ideas about economic growth and all the baggage that goes with it. The implications for our politics are profound.

Economists sometimes like to portray their discipline as the description of immutable laws. They show tables of statistics (or rather graphs – see above) going back centuries – with uniform metrics such as income, prices and productivity. The idea is to present the economy as a continuum, even if as the world behind it changes. This might lead us to think that the tools of economic management are of timeless relevance. What if Keynesian demand management had been discovered earlier! But this is really an attempt to project the present back into history. The world has been changing profoundly over the last three centuries and the economy with it. With these changes come changes to our ideas of what economic management is about, and politics with it. But the process is slow and complex, and it can be hard to appreciate it at the time. That’s why I think it is helpful to paint a picture of how things have changed in the past, to give an idea about how things might be changing again now. I like to rationalise the past into a series of epochs – but, of course, each each moved seamlessly into the next. This narrative is based on how things were in Western Europe in particular, and by extension its colonies in North America.

The first epoch was the Age of Subsistence, from Medieval times into the 18th Century, which was overwhelmingly agricultural and marked by stasis. There were important technological developments, and the changes to trade patterns also had important impacts. Textiles, mining and iron working played a role, leading to occasional local booms and some nice stone buildings for us to see today. There was sufficient agricultural surplus to support a number of cities and towns. But the overall picture was fairly static and based on agriculture, mostly of a subsistence nature. The vast majority of people worked on the land in a very low-productivity agrarian economy. The big political idea was that people should know their station and not get beyond themselves. The idea of abolishing poverty was considered to be delusional nonsense. God created a world ever divided between the aristocratic rich and the peasant poor, and that was that.

Then came the Industrial Revolution, which was initially based on textiles and agriculture. Farming became more efficient, not so much directly from changes in technology, as from the application of scale economies, with enclosures and evictions. Agricultural surpluses could be moved by canal, and the cash economy expanded. Labour moved to textile mills, where mass production techniques were developed. Also at this time slave labour was used in overseas colonies to produce such products as sugar, tobacco and cotton. Trade grew in importance and a substantial middle class emerged. Social mobility became more of a feature of society. A lucky few managed to climb from working class to middle class; an even luckier minority of middle class people aspired to the aristocracy. But the labouring classes saw no improvement in their lot. There was no move to reduce poverty. But the new middle classes questioned the ways of the governing elites and this had a profound political impact – most notably be the American and French revolutions – but also with such things as the anti-slavery movement in Britain.

This moved, in the 19th century, to the Age of Heavy Industry. This saw the rise of railways and steel. Infrastructure (railways, ships and sewers for example) and armaments became the centre of attention. Right though until the middle of the 20th Century, economic success was measured in terms of the rise of heavy industry. Hermann Göring’s statement that “Guns will make use powerful; butter will make us fat,” summed up the way that most people thought about economic policy. Stalin’s building of Russian heavy industry at the cost of millions of lives was generally considered to be tough but rational. But improving the lot of the poorest did start to command political attention, as working class movements rose. Sanitation improved, free education was offered to all, and a welfare state started to emerge. This age culminated during the Second World War, which was largely decided by industrial production. But it quickly morphed into the Age of Light Industry. Many of the technological developments forged in the war, such as plastics, turned out to have applications in consumer products. And the need to switch away from war production offered the opportunity to greatly expand the production of mass market consumer goods. Pretty soon mass consumption was considered to be the top priority for the political economy. The concept of economic growth was developed to reflect this and the prospect of abolishing poverty. The West won the Cold War because the Soviet empire could not compete in the production of consumer products, and its leadership lost confidence in their raison d’être.

Something else profoundly important developed alongside the consumer economy: the rise in the role of the state. The state greatly expanded in wartime, intruding into all aspects of life. People noticed that rationing meant that austerity in the nation as a whole did not mean that the poor had to starve – indeed nutrition for the poorest improved in Britain. This vindicated a role for the state in providing a social safety net, with health insurance, unemployment pay, expanded pensions and so on. Productivity was high enough for agriculture and consumer goods that there was room for a growing state sector. Politics became managerial, with politicians promising to offer prosperity to all. Social mobility exploded.

But the world has moved on. Many noted a major change in political and economic thinking in the 1980s, following he economic travails of the 1970s. There was a push-back on the growth of the state and on organised labour. De-industrialisation started to take hold as productivity continued to advance in manufacturing. The rise of Asia, starting with Japan, offered gains from trade as cheaper manufactures could now be imported. But growth in consumption still dominated expectations. Manufacturing industry was still considered to be the core of the economy, much as agriculture would have been in the 18th Century.

To understand how things have changed, consider a few things about the world around us, in developed economies. First are the signs of saturation in consumer demand. Of course there are plenty of people struggling with the basic necessities – but they are a minority. Meanwhile people buy cars absurdly over-specified for their needs, and leave them parked outside their homes doing nothing most of the time. People buy clothes to wear once or twice before they are discarded. Much of people’s wealth is spent chasing things that are not made – notably land for homes, even if just for temporary residence rights. A lot of “consumption” is in fact about the acquisition of status symbols.

Then there is the idea that consumption is actually bad for us. Environmental degradation is one example; climate change is another. And then there is health. Highly processed foods, where agriculture and manufacturing meet, are clearly damaging to our health, and one reason that life expectancy is now in decline. And yet to economists they are ideal commodities: based on high productivity and promoting over-consumption, and thus with beneficial economic impacts. Better off people increasingly choose products that are healthier with reduced environmental impacts (though still prone to massive over-consumption) – but these imply reduced productivity – the biggest crime there is in the Age of Light Industry.

And then there is changing meaning of “quality of life”. Once this meant being able to consume commercially produced things to the maximum extent. But increasingly this is taken to mean working less hard. People take earlier retirement if they can – notwithstanding that many are physically able to work for longer (your blogger is guilty as charged). The recent pandemic has led to an explosion of demand by employees to work from home – even if it means being paid less. Evidence mounts that this reduces productivity, but most employers are forced to compromise. Working longer – or expanding the workforce – is, after raising productivity, one of the core strategies of a growth economy, and it is being thwarted.

Consider health care too. This comprises a growing share of the economy (in some places it employs more than manufacturing, I suspect). But it is is peculiarly ill-suited to the sort of quantitative analysis that likes to see things in terms of output and productivity. New therapies are developed; these solve problems that were unsolved before – but often require a greater level of inputs. Demand is insatiable; the share taken of the total economy grows.

And economic growth is slowing, much to the worry of economists. Many of these point admiringly to the more “dynamic” American economy – but Europeans question whether small holiday entitlements, poor life-expectancy, terrible inequality, and high environmental degradation are actually worth it. What if slow growth is the result of the freely made choices by those welfare-maximising agents, beloved of classical economists? Economists and politicians have to adapt to the reality – rather than try to make people behave according to an outdated model. This was the terrible strategic mistake made by British prime minister Liz Truss’s catastrophic regime.

The overall narrative is easy to see if you are willing to look. Technology has so advanced, and environmental imperatives have so grown, that a focus on people’s true interests and wellbeing does not involve increased levels of consumption – and will often lead to reductions. Investments in new, cleaner energy infrastructure will create jobs but not lead to economic growth in the sense that we have understood it since 1945. But where this leads is harder to discern. Politicians are right to worry about the lack of growth. Demand for public services remains high, but the economic model for managing supply and demand is breaking down. The current model is that people pay taxes, which limits demand for private sector goods, allowing economic space for public services. But if demand for private services stagnates or declines, while that for public services expands, this means that taxes have to rise. That is a political challenge – the connection between what you personally pay in tax and how you personally benefit from publics services is a weak one. That becomes even harder if the size of the workforce stagnates or declines because people would rather not work, and have sufficient savings to fulfil that desire.

So far politicians, economists and, indeed, the public at large cannot imagine a way of meeting the crisis in public services without stoking economic growth. The Labour leader, Sir Keir Starmer, says that growth is at the heart of his strategy for government. But it won’t work. And this fact, and its consequences, will dominate politics in the coming decades.

Advances in technology give us the opportunity to continue advances to human wellbeing, even while reducing harmful impacts on the environment. But assuming that this will come abut through economic growth is mistaken. We need a new language to describe the economy. In future posts I will try to develop ideas about what his actually means.

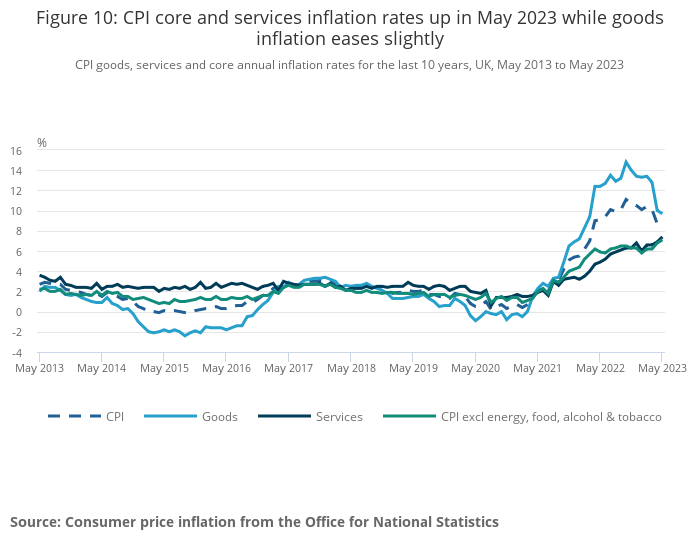

Yesterday Britain’s state statistical agency, the Office for National Statistics, released inflation figures for May 2023. The headline figure of 8.3% was unchanged from April, but the “underlying” rate (CPI excluding energy, food, alcohol and tobacco in the above chart) continued to rise. Commentary on the BBC Today programme and in today’s Financial Times was notably dark. There seemed general agreement that the Bank of England would have to increase interest rates, and keep them higher for longer than previously expected. And indeed the Bank raised rates by a full 0.5% later in the day; 0.25% had been widely expected.

Until now two overlapping narratives about inflation had been prevalent among the commentariat. The first, call it “global shock” is that the rise in inflation since 2021 has been essentially a temporary one – driven by higher oil and gas prices, and exacerbated by the war in Ukraine, which affect all developed economies. The thinking was that these would either reverse or get baked in (i.e., drop out of the 12 month statistics). When the prime minister Rishi Sunak set out his five main priorities at the start of this year, halving the rate of inflation came top. The general view at the time was that this target would be achieved without any government action so that the Mr Sunak could take credit for a statistical artefact. While it was popular to criticise central bankers for thinking that inflation would be “transitory” when it first started to rise, it hasn’t stopped many people from thinking that themselves subconsciously. The second narrative, “supply shock”, was a bit more subtle: it was that inflation this time was a supply-side phenomenon and not resulting from excessive demand. The upshot is that the solution is not to crimp demand by raising interest rates, but to wait for the supply side of the economy to correct – indeed raising rates would only reduce the investment needed to fix the problem. The supply side issues referred to included the energy crunch, but also the repercussions of the covid-19 pandemic on supply chains.

These narratives are breaking down, especially as the rate of price increases in services persists. This seems directly related to rising levels of pay, which have also come through in the statistics. While some academics suggest that the “wage-price spiral” of 1970s fame is no longer a major dynamic (see here in The Economist), there seems to be what The FT’s Chris Giles calls a “ratchet”. Pay rates increase in response to energy prices, and this feeds into service costs, which in turn might lead into further payrises. Meanwhile supply side issues do not seem to be sorting themselves out; labour shortages are ongoing. This seems to be particularly strong in the UK. Various things catch the blame for this: EU nationals going home after Brexit; lack of flexibility in the post-Brexit immigration system; more chronic illness; people retiring earlier than expected: take your pick. What is now clear is that if inflation is to be limited something has to be done to limit demand.

At this point the economic illiteracy of the political class becomes evident. Many hang on to the idea that responsibility for managing inflation rests with the Bank of England alone. Some seem to believe that this can be done in some kind of immaculate way without hurting economic growth, or at any rate that there was an opportunity to do this if the Bank had reacted to initial energy price shock sooner. The previous Prime Minister, Liz Truss, seems to have held this view, and now a number of government advisers are briefing the press along these lines. In fact the Bank was following a firm consensus shared by the government, and the political stink that would have arisen if it had tried would have been a sight to behold, with the “global shock” and “supply shock” narratives being widely trumpeted. Now at least people are understanding that “if it isn’t hurting, it isn’t working”, an idea that was widespread dung the last inflation crisis in the 1990s. And yet the hurting seems to be concentrated on one particular group: home-owners with mortgages. Well there are others: public sector workers, where the government is fighting hard to limit payrises, and people living in rented accommodation, as rents are on the rise (although the reasons for the rental problems seem to be complex, with interest rates only one factor). Many others, such as people who own their homes with mortgage paid off (like me) are under no special pressure. All this does not seem to be especially fair.

The political debate around this is laughable. Labour’s priority is to try and blame the crisis on the Conservatives. And yet they cannot point to a clear “told-you-so” moment to show how they might have done anything differently. Neither are their ideas on tackling the crisis now conspicuously different. They give the impression that they would be easier on public sector pay, but not how they would manage the fiscal consequences of this. Their very limited tax raising ideas to cover extra spending would do nothing to manage demand in the economy. The Lib Dems suggest a hardship fund to help the most pressurised home-owners; this is not as mad as the thoughts of some Tory backbenchers to offer tax relief to all people with mortgages – but would still need to be balanced with a tax rise that hurts demand, which various forms of tax on excess profits would not. Supporters of Liz Truss would focus more clearly on various supply-side problems, like the need to build more housing, but wreck this with their advocacy of lower taxes. Instead of this hot air, two particular ideas should be current in political circles.

The first is that we could manage the demand side of the economy more fairly through raising taxes. By this I don’t mean the various tax gimmicks that opposition parties try out which could raise funds without hurting most people (windfall taxes, taxing rich people’s perks, non-doms, and so on) – as the “if it’s not hurting, it’s not working” mantra applies here too. It means putting up taxes on the big three – income tax, VAT or National Insurance. In practice, that means income tax. National Insurance lets rich pensioners off; VAT is too hard to explain when trying to fight price raises, at its short-term effect is to increase inflation. To be fair, the government is raising income tax by refusing to raise allowances and thresholds, causing “fiscal drag”, though they don’t want to draw attention to this. But more needs to be done – and if it was, there would be less pressure on interest rates.

The second idea is to suggest that inflation might not be such a bad thing after all, if it means a rebalancing of pay to those currently earning less. This would flow from policies to limit immigration of lower-skilled workers, for example. The corollary of this would be to temporarily raise the Bank’s inflation target, and to find ways of cracking down on profiteering by businesses (so that the benefits of laxity went to the workers, not business owners). That, incidentally, is a bit harder than it might seem, as one of the side-effects of inflation is to create false profits from the time lag between paying for inputs and billing for outputs. That would be a distinctly socialist approach, but surely no madder making mortgage holders bear the brunt of the fight against inflation. A bit of dialectical debate around this idea, and that of tax rises, would do no harm. But both are politically toxic.

High inflation, and increasing hardship for a growing number of people, is the result of multiple problems in the British economy. Strong political leadership will be needed if the outcome is to be a fairer society – which it could be. Alas no such leadership is in sight.

“A sensible politcal debate” is surely an oxymoron. Politics is a battle of personal ambitions in which popular prejudices provide the most useable ammunition. If you catch two politicians having a sensible debate, it is away from public attention, about an issue with no real salience. Immigration is an issue of high political salience – and always has been, so we shouldn’t wonder that so little of what is said by politicians makes any sense in the round. But in the end effective policy needs to be based on reality, and a sensible debate is needed to tease that out. Immigration is a case in point.

Immigration is currently moving up the political agenda. This is in spite of the fact that the leaders of none of the major political parties would rather talk about other things, and opinion polling shows that it is relatively low on the list of public concerns. That is because a group of conservative politicians see it as an opportunity to create mischief and further their political careers. The proximate cause are statistics that show immigration at record levels – though these statistics are highly unreliable as data collection is weak. The numbers have been driven up Ukrainian and Hong Kong refugees, the need for universities (and the country at large) to extract money from foreign students, and widespread labour shortages. Each of these causes seems to be understood by most of the public. So what’s the fuss?

There seem to be two main, mutually supporting strands raised by conservative politicians (with Labour leaders happy to echo them in their bid to show their conservative side): cultural and economic. Immigrants are usually culturally distinct (we can argue whether this is true of Australians…) – with different languages, religions and customs, and often maintain distinct communities. This is blamed for corroding traditional British culture. There is more than a tinge of racism here, though it is notable that many of the the leading public conservatives are themselves from ethnic minorities, and these ideas resonate with settled ethnic minority communities. There is plenty of irony here. Immigrants are keeping the churches full and often have conservative social values. One leading conservative politician claimed that immigration was leading to the declining number of people professing to be Christian, when the opposite is true. Of course this person (Nigel Farage) was seeking to exploit the trope that Western countries were being taken over by Muslims. It is easy for cosmopolitan liberals to laugh at all this, so many are the inconsistencies, but the message resonates well with older and less-educated people. There is a real conflict here between the cosmopolitans, typical of larger and more successful cities, and nativists, typical of more rural areas (though my own rural abode of Sussex is pretty cosmopolitan, it needs to be said) and smaller towns. If you take the Brexit referendum as an indictor of how the two outlooks divide (and it is more complicated than that) – then the country is split fairly much 50/50. It currently helps that, apart from the Ukrainains perhaps, the bulk of existing migrants tack onto communities that are already well established here – Indian, Chinese and Nigerian in particular.

Because of the clash of cultural attitudes, and the need to draw support from both sides, perhaps, most politicians choose to make their main arguments on immigration in terms of economics. It is said that excessive immigration is causing public services to be overstretched, exacerbating housing shortages pushing up property and rental costs, and pushing natives out of decent jobs, or at least pushing the level of pay down. The public services argument is the least serious. Public services are often amongst the most dependent on immigrant labour, and would be under even more strain if immigration was reduced. But a local influx can cause problems, and the system can be slower than it should be to adapt.

The argument on housing is more convincing. Pretty much everybody agrees that the supply of housing is failing to keep up with supply – though new housing developments seem to be popping up everywhere I travel to. After that vested interests take over, and it is very hard to get an objective take on things. One group of people blames restrictive planning laws which stop new homes being built, especially on rural and green belt land. The other side says that this would simply give developers carte-blanche to build lots of poor quality houses in ecologically vulnerable beauty spots, together with some high-end properties to act as stores of financial value for footloose foreigners. Clearly high levels of immigration make the problem worse – but the middle ground between developers’ search for an easy profit and nimbies trying to protect the value of their existing properties is largely uninhabited – and draws little serious, well-funded research. Economists tend to side unthinkingly with the developer lobby. Politicians may talk as if they are in the middle ground, but lack well thought-out policies that might do any good, and I’m practice end up at one of the extremes. Arguments over immigration just add grist to the mill. It is very hard to understand the implications of immigration strategies for housing without having a clearer idea of about housing strategy. But it clearly doesn’t help.

What about immigration and jobs? Recently changes as a result of Brexit caused a shortage of lorry drivers. Their pay shot up as a result; training schemes were upgraded, and more locals are now taking up the work. This is exactly how conservatives arguing for lower immigration say things should work. Using immigrant labour is an easy shortcut – but we would be better off we raised pay and brought more locals in to do the jobs. This is the vision conjured up by the Tory former leader Boris Johnson at the last election. But there’s a problem. This should mean that public sector wages need to be raised to help draw more people into the workforce. And yet the government wants to do the opposite: to use inflation to reduce real levels of public pay, and use the resulting surplus to fund tax cuts. They do this in the name of reducing inflation – but offer no long term solution to the problem of public sector pay. In fact a rebalancing of the economy in favour lower paid jobs will surely result in a degree of of inflation. It may also require taxes to be raised. The issues are quite complicated here, but a limited supply of labour creates something of a zero-sum game. Raising wages for the lower-paid is going to hurt somewhere.

Politicians sometimes talk about the need to improve training so that more locals can do jobs where we currently need immigrant labour. This clearly won’t work for things like fruit-picking, but is more convincing for doctors, nurses and social care workers. The problem here, as Stephen Bush of the FT points out, is that skilled labour is mobile, and the freshly trained workers will simply gravitate to where the best paid jobs are – which are often not in the UK. It is putting the cart before the horse. As the case with lorry drivers shows, if you fix the pay issue first, training is a much easier problem to solve.

The big, unspoken issue lying behind the fuss, is the country’s demographic development, with retired people taking up an increasing share of the population, while at the same time driving up demand for public services. Immigration is the obvious answer to this problem, though not in the long term, as the immigrants themselves will retire. If immigration is not the answer, then what is? Politicians place hope on increased productivity – but for a number of reasons this will not cut the mustard. The areas where productivity needs to advance to make the sort of impact required – in health care and social care services – seem to be those with the fewest practical proposals. Indeed, health and safety worries tend to push them in the opposite direction. Big investments in hi-tech factories may be a very good idea, but they will make little difference to economic growth overall, and impact the labour market even less.

The idea that the country should limit immigration is a perfectly respectable one. But it has a cost – we must pay more for critical services that are subject to labour shortages. That will involve a rebalancing of the economy and some painful economic adjustments. It would help if more people would talk about what this, exactly, means.

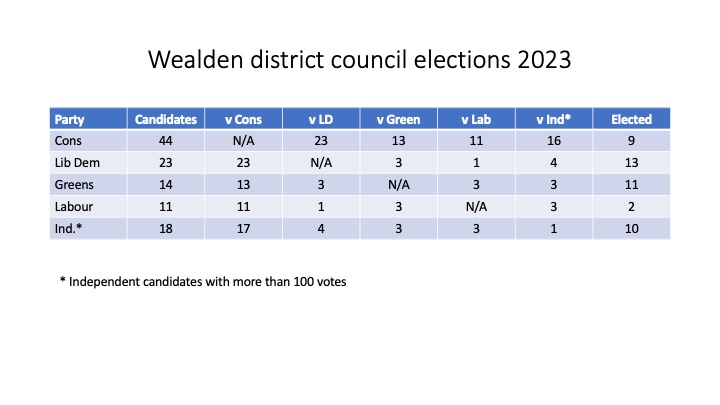

Such is the paradox of the information age. Massive amounts of information from across the globe is at our fingertips, and we can now use AI tools to retrieve it with startling efficiency. But news reporting, especially local news reporting, has collapsed – so many, many interesting things are liable to escape our attention because they will never get into to the accessible database. There has been a wealth of reporting on last week’s local election results in England. But many interesting, and important, local stories remain unremarked. Such is the case in my local area, with the district council elections of Wealden in East Sussex – and arbitrary bureaucratic agglomeration of villages and small towns, whose main centres are Uckfield, Hailsham and Crowborough, each of roughly equal size.

The first point to make about this is that I wasn’t involved in these elections, in spite of being a party member. I haven’t talked to any of the actors since long before the campaign started. My reporting is based simply on the results published by the council. I hope to find out more later – but I’m not minded to harass exhausted newly-elected councillors who have important decisions to make about running the council. I’m a blogger, not a journalist.

It was the first British public election since 1979 in which I did not vote for the Liberal Democrats, or one its predecessor parties. That was because they did not field a candidate in my ward. There were only three candidates: a Conservative, a Green and an independent who did not put up much of a visible campaign. I voted for the Green candidate, Christina Coleman, who won with 64% of the vote against the Conservative incumbent councillor, Roy Galley, who had won in 2019 with 59% of the vote, against just a Green candidate. Ms Coleman increased the Green vote from 523 to 1,107, while Mr Galley’s vote sunk to 545 from 749. As I searched through the results, I found that this outcome was not untypical. The Conservatives contested wards opposed by typically only one other party. And they lost badly, sinking from 34 councillors (out of 45) to just 9, behind both the Lib Dems (13) and Greens (11). This was a shocking result in a part of the Blue Wall that is so blue that most people don’t regard it as politically competitive. This bespeaks serious trouble for the Conservatives. It is hard to exaggerate the degree of disgust with the party amongst most of my neighbours, whom I would describe mostly liberal conservatives. One Conservative inclined neighbour is even more unforgiving of the Liz Truss episode than I am.

But that is unremarkable. It has been picked up by the main media commentary. What is remarkable was the degree of cooperation amongst the Conservatives’ opponents, and how well this worked. To put a bit of substance behind this story I have analysed the detailed results in the table above. This is all my own work and it’s possible the odd error has crept in. First, some basics to help understand the figures. There are 41 wards, four of which elected two councillors, and the rest just one. One was uncontested – the Conservatives were elected unopposed. The Conservatives contested all the wards except one (where an independent stood, and lost, against a Green). In the analysis I have tried to exclude candidates without serious backing or a campaign. I judged these to be independents who did not manage to gain 100 votes, and minor parties (though in one ward there was a Reform UK candidate, and in a another a pair of Ukippers, all of whom received over 100 votes); I have left in all of the Labour candidates, although one failed to reach 100.

The Lib Dems put up 23 candidates, doubtless so that they could claim that they could theoretically win a majority on their own. But they were opposed by the Greens in only three cases, and Labour in one, with “serious” independents in four. Eleven of the Lib Dem candidates faced no other serious opponent than the Conservatives; they were all elected – but only two others were. The Greens put up only 14 candidates – nine of these faced only one serious opponent (well, 10 if you exclude a weakly supported Labour candidate) – all (ten) of these were elected, along with one other. Three Labour candidates out of 11 were given a clear run against Conservative candidates; none were elected. Two Labour candidates were elected in three-cornered battles with Conservatives and independents (including a split result in a two member ward) – their first councillors in the district. The independents are by their nature not a coherent party, so the analysis means less – but their 18 serious candidates were involved in only four straight fights – three against the Conservatives (which they all won) and the lost fight with a Green. There were 13 three or four cornered contests: the Conservatives won six of their councillors here. These six, the two straight fights with Labour and the one uncontested ward were all the councillors they won. They won no contest in a straight fight with Lib Dems, Green or Independents. In two case of the more complex contests, the Conservatives prevailed with under 40% of the vote. In only three cases Greens and Lib Dems ran candidates against each other – the Conservatives won in two of them (with under half the vote), with the Greens winning the third comfortably with the worst Lib Dem performance of the day.

So far as I know there were no formal pacts – if there had been, the picture would have been a bit tidier. But cooperation is evident, and, as a device for winning against Conservatives, it proved highly effective – but less effective where Labour were putting up the candidate. How far can we extend the conclusions to a general election? Local and national elections are different – but the main problem for the Tories in Wealden was their unpopularity at national level. Their Wealden administration is not particularly unpopular, though no especially popular either. This suggests to me that an electoral pact between the Greens and the Lib Dems could turn some seats in the Blue Wall unless the government can seriously scare voters about the prospect of a Labour-led government. Wealden borough closely corresponds to a parliamentary seat, also called Wealden, which is very safely for the Conservatives (the Lib Dems edging ahead of Labour into a distant second) – but this all changes when new parliamentary boundaries come in. Such a pact would follow one made in 2019, but could be much more effective if voters are less scared of Sir Keir Starmer as Labour leader than Jeremy Corbyn.

But it would be very hard to bring Labour into such a pact. Many former Conservative voters will vote for the Lib Dems or Greens (somewhat ironically since the Greens are closer to Corbyn’s Labour than Starmer’s), but draw the line at voting Labour. So there is much less in such a deal for Labour than the other parties, and it would be a major distraction from Labour’s main campaigning focus. Also Sir Keir is setting his face against electoral reform (which would be another distraction for him), which reduces the attraction of Labour to Lib Dems and Greens.

In the right circumstances electoral pacts work. Given the severe distortions imposed by the current electoral system I would have no qualms about my party entering into such a pact.

Politicians have to navigate two worlds: that of politically correct official policy and the respectable disagreements with it, and the world of their committed supporters where more extreme views are common currency. This happens in all parties. Liberal politicians have to restrain and suppress views on such topics as Brexit and immigration, for example. This does not stop politically incorrect views being widely disseminated in mainstream media, of course, but politicians must be very wary of publicly supporting any such views. Two episodes which broke over the weekend illustrate this.

The first was that of Dominic Raab, who resigned as deputy prime minister and Justice Secretary, after a report into accusations of inappropriate behaviour – bullying – in the management of civil servants, which upheld some of them. Mr Raab came out swinging: he suggested that the threshold set for bullying was set too low, and would make the task of ministers implementing their promises to electors impossible. He also suggested that some civil servants were undermining the government because they disagreed with its policies. These complaints were taken up by parts of the press, notably The Telegraph. It was soon being suggested that the complaints were orchestrated in order to remove a politically contentious but hard-working minister – and that others would receive the same treatment.

The prime minister has remained silent on the issue; opposition parties have piled in to condemn Mr Raab, with the Liberal Democrats even suggesting that he resign as an MP. On the face of it, Mr Raab’s arguments are hard to sustain. Most of the specific complaints made by civil servants (six out of eight) were not upheld – but there were two examples that the report’s author, employment lawyer Adam Tolley, viewed as too extreme. It would be easier to accept Mr Raab’s assertion if all the complaints had been upheld. The bar Mr Raab seems to want is high indeed – physical intimidation. Others point out that Mr Raab’s record of achievement in office is weak, compared to others with similar politics. I have spent many years in a professional management environment and have no sympathy with what Mr Raab is suggesting. There are good and bad ways of getting the people you work with to do what you want; Mr Raab clearly opted for the bad far too often. I am pretty obsessive about fonts and formatting (apparently one of the issues that Mr Raab complained about) – but as a manager I just had to let go, as the topic didn’t matter all that much in the end.

Still, Mr Raab is getting a sympathetic hearing in many places, and not just The Telegraph. But this is not politically mainstream. One survey suggests that most people claim to have experienced bullying by their superiors at work. I have worried that bullying behaviour by managers is so commonly portrayed in television and film dramas that people think it is how management is done – but this is doubtless trumped by direct personal experience, where people meet good management technique as well as bad. The FT’s Stephen Bush suggests that political careers tend not to provide such exposure to good management practice, though, and perhaps that is why politicians so often fall into Mr Raab’s trap. It is easier to see how the idea of the civil service undermining government policy has currency, though. The idea of a civil service “blob” is popular amongst conservatives; doubtless socialists who have made it as far as government office feel similarly. Passive-aggressive behaviours are common in all organisations, though, and the more radical your ideas are, the more of it you will get – as I know full well from direct experience. It is something competent managers develop techniques to manage, and less competent ones get paranoid about. But such conspiracy theories are the currency of activists and not the political mainstream.

Diane Abbott’s case is perhaps a bit more interesting. Ms Abbott is a long-standing Labour MP, elected in 1987, as the first black woman elected to parliament. While she can be a bit eccentric, she is clearly an intelligent person, and one who has suffered mountains of misogynistic and racial abuse. Her problems arose from a letter to The Observer newspaper, in response to this article by Tomiwa Owolade. It is worth getting the context of this episode right. Mr Owolade led off with this anecdote:

I was a sixth-form student and talking to a girl who told me with utter confidence that “white people can’t be victims of racism”. Racism is about power and privilege. White people have power and privilege. Black people and Asians don’t. This means that only the latter group can be victims of racism; racism is the exercise of power and privilege against people of colour.

Tomiwa Owolade, The Observer 15 April 2023

He describes how at first he accepted this point of view, but that he came to reject it: life is much more complicated than that (‘not black and white” as the title to the article has it). In evidence he discussed a recent survey of people’s experiences of racist abuse. This found that both Jews and Irish Travellers, people often defined by black people as “white”, were more likely to experience such abuse than black or Asian people. The survey even found that white Irish people suffered more racial abuse than black Africans or Asians. He also pondered the fact that in the survey most black and Asian people did not claim to have experienced racial abuse at all. Of course a survey such as this is not conclusive evidence by itself, and actual experience of abuse is only one explanation of the way people answer such questions: but it is clear that Jewish people, and especially Irish Travellers, experience a lot of abuse.

This was, apparently, too much for Ms Abbott, who clearly agreed with the girl in Mr Owolade’s anecdote, and defines Jews, Travellers and Irish as white. She has since withdrawn the letter (and apologised for its content which she described as an early draft sent by accident), and I haven’t found a version of the full text to link to. These are the sentences that have been most widely quoted:

It is true that many types of white people with points of difference, such as redheads, can experience this prejudice. But they are not all their lives subject to racism. In pre-civil rights America, Irish people, Jewish people and Travellers were not required to sit at the back of the bus. In apartheid South Africa, these groups were allowed to vote. And at the height of slavery, there were no white-seeming people manacled on the slave ships.