My latest Substack past, here, has seen more engagement than anything I have posted recently. It’s impossible to guess what will evince a reaction, and what a yawn!

These theme may be a familiar one to my regular readers, but I seem to have presented it in a more engaging way.

05/07/2024. London, United Kingdom. The Prime Minister, Sir Keir Starmer and his wife Victoria arrive at Number 10 Downing Street upon his appointment. Picture by Kirsty O’Connor/ No 10 Downing Street

Sir Keir Starmer, Britain’s Prime Minister, can be summed up in a single word: Focus. He is learning the problems that this characteristic brings. His focus on winning the election on 4th July has made his life much harder now that he has won. Labour has made an awkward start to its term of office.

In government Sir Keir’s focus is on five “missions”. This is an admirable approach compared to the chaos of Conservative governments, especially since 2016. We can quibble about the design of those missions: number one is “kickstart economic growth”. Growth makes a poor target: it’s both a bit like targeting happiness, which is something that happens when your are trying to achieve something else, and a bit like targeting the birth rate, which just isn’t under state control. It is under this heading that housing is being tackled: much better to have targeted housing specifically, surely. Social care doesn’t make it into the five – which cover the energy transition, law and order, education and the NHS (or in fact health) – but which of the others would you drop? Neither does immigration, which would have featured in any Tory big five – but that is more understandable. Focus is integral to achievement,- but it comes at the expense of risk management. A lot of the skill of management is learning how to balance the conflicting requirements of focus and risk management. Sir Keir must not be too relentlessly focused – he needs to have a strategy for dealing with the many other issues that have the potential to derail. He needs to use trusted colleagues for this.

What Sir Keir had clearly hoped was that the sight of a government clearly focused on achieving the nation’s priorities would present such a contrast to the previous government that he would have a prolonged honeymoon – especially as there is no coherent opposition. That has not been so. The summer’s big unforeseen event was the rioting that followed the Southport murders – but these played to Sir Keir’s strengths. A strict no-excuses crackdown was what the public wanted and this was delivered without hesitation. But from this emerged a big problem: neither he nor his most important colleague, his Chancellor of the Exchequer Rachel Reeves, are good communicators. They are wooden in their presentation and in their responses to questions. This has not helped them in their presentation of bad news about the government finances, the need for continuing austerity, and in particular the cancellation of the winter fuel allowance for all but a few state pensioners, just as fuel costs were rising again. They are blaming this on the previous government covering up a black hole in the nation’s finances -but this is coming across as insincere. Not without reason.

The problem is that the “black hole” in government finances is not at all surprising – so acting surprised looks fake. Throughout the election campaign the Institute for Fiscal Studies, a well-respected think tank, complained that all the parties were painting too rosy a picture of the nation’s finances. It really wasn’t hard to see why. The previous government was trying to use inflation to squeeze public sector costs – and noticeably force down the real pay of public sector workers. On this basis they fairly transparently cooked official forecasts that they could make cuts to National Insurance – even after they had tried to raise the tax in 2022. But Labour were silent about all of this, choosing not to challenge the Conservative’s general policy direction. Both parties seem to have been obsessed by the thought that the 2024 election could be a repeat of the one in 1992, where the Tories successfully built a campaign on “Labour’s Tax Bombshell” that turned a seemingly inevitable victory for Labour into defeat. Labour promised not to raise any of the main taxes (Income Tax, National Insurance and VAT), matching a Tory promise and said they would match Tory spending projections except in a few specific places. They were evasive on the clear implication (highlighted by the IFS) that this meant austerity in most aspects of government spending. Sir Keir’s focus was on winning the election with an outright majority, and he wanted to leave nothing to chance. If he was being dishonest, then he was no more so than the Tories, the thinking g seems to have been.

But, as my mother used to say, two wrongs don’t make a right. Labour could have been more honest about the state of the nation’s finances before the election, and they weren’t. The focus on winning the election has made the task of government much harder. Sir Keir has been desperate not to repeat the Tory habit of over-promising and under-delivering, and has been caught out over-promising. He is, of course, trying to pin this on the previous government, in the manner that David Cameron’s coalition government pinned the blame for its austerity policies in 2010 on the previous Labour one. But Mr Cameron, his Chancellor David Osborne, and even his Lib Dem deputy, Nick Clegg, were all much better communicators than Sir Keir of Ms Reeves (not that this did Mr Clegg any good…). Their hopes rest on the fact that with the next election four or more years away, some more positive events may have overtaken this difficulty.

I am disappointed. I had allowed myself a brief moment of hope. The speed with which the government settled the various public sector wage claims seemed to show a degree of imagination. They must have overcome firm Treasury pushback that “we can’t afford it”. But the better country that they want to bring into being features a happier public sector workforce, and better pay for the bottom and middle quartiles, and less dependence of cheap overseas immigrant workers. Squeezing public sector pay, with no plan for when any catchup might happen, is just takes the country further away from this goal. This is the reason I think that Jeremy Hunt, Ms Reeves’s predecessor, was one of the most disastrous Chancellors of recent times. He swallowed the Treasury logic on payrises and then made things worse with tax cuts.

But that flicker of hope has been suffocated. No evidence of such a degree of long-term vision has emerged. Instead the story was that the urge to settle the disputes was because they were unpopular and a distraction, and the previous government could be blamed. I was particularly disappointed that the government allowed the Treasury to defer the previous government’s plan to tackle the growing social care crisis, for the nth time. The government has to stick to its promises on tax, and social care didn’t make it onto the big five priorities. But the long-term consequences are not good, and some kind crisis is in the making. Labour’s focus on the election is making the challenge of decent long-term government harder.

Still, it isn’t all bad news for the government. None of the contenders for the Conservative leadership look capable of leading a revival for that party. The rift on the right, with the success of Reform UK, looks as if it will do for Labour what the rift on the left did for Mrs Thatcher in the 1983 and 1987 elections – enable landslide victories on the basis of lacklustre vote share. And the Lib Dems show some of the same problems as Labour. A relentless focus on doing well at the election at Tory expense leaves them ill-equipped to tackle Labour. The prospect that Sir Keir will get a second term remains good. The mandate that he seeks at that election will be critical to the success of his project overall. He needs to give himself much more room for manoeuvre.

PS Other commitments mean that this will be my last post for at least a couple of weeks. I plan to resume after the Lib Dem conference with my thoughts on what that party should do next.

Government finances are under water. OK, a weak link but I’m bored of AI images and public domain photos. Bosham in Chichester Harbour this weekend, by my own hand.

Taxation and public spending is very much on the political agenda here in Britain. The Chancellor of the Exchequer, Rachel Reeves, is claiming that there is a £22 billion black hole of unfunded spending commitments in the government finances, left by a Conservative government addicted to brushing problems under the carpet. There is much talk of how her Labour government might raise taxes to plug this hole and meet expectations of improvements to public services and the social safety net.

This makes it a good time to ponder the economics of all this. Public debate encourages us to think of the state’s finances in terms of a household budget: public spending must be covered by taxes, or else the national debt gets out of control, which in due course could mean throwing the country to the mercy of foreign creditors, or burden future generations. This narrative has the merit of being easy to communicate and sounding like common sense. Try telling voters that this is not how things work, and they will immediately become suspicious. The US Republicans, to my knowledge, are the only politicians to have succeeded with a different narrative: the so-called “Laffer curve”, whereby tax cuts pay for themselves through economic growth. Former British Prime Minister Liz Truss tried this out on the British public in 2022, but it went very badly. Her supporters argue that his was actually through bad luck – but most politicians now treat the idea of “unfunded” tax cuts or spending commitments as politically toxic, as well as economically unwise.

The Laffer curve is in fact just one argument against the household budget narrative – but it is not a huge departure from it. Households may borrow to invest, so states should be able to so as well. If a budget deficit leads to a future increase in revenues, or lower costs, then surely it is sustainable? Labour tried to make this case with a proposal for massive investment in clean energy infrastructure – but lost their nerve as the general election loomed. Joe Biden’s administration is actually implementing such a programme in America, but the public there are resolutely sceptical. You have to believe that the future benefits are for real – and the public is generally unbelieving. Not without reason, as the processes of accountability are weak.

A further, and well-established, argument against the household budget narrative might be called the Keynesian critique. This follows the argument originally put forward by the great economist Maynard Keynes, after stringent budgeting by governments during the Great Depression of the 1930s made things worse. If there is spare capacity in the economy – a typical feature of recessions – then it makes sense for the government to run a deficit to raise demand and employ unemployed workers, creating a virtuous circle of growth – and stopping a potential doom-loop of savings leading to reduced demand leading to further savings. Governments should use taxes and spending to help manage overall demand, to ensure that the economy runs at an efficient level of capacity. This idea is very popular on the political left, who generally assume that the economy is always working below capacity – but it is not always easy to tell if there is spare capacity. Many people thought that high unemployment in the 1970s meant that there was spare capacity then – but generous fiscal policy simply seemed to stoke inflation – “stagflation”. In fact the escalating price of oil, amongst other things, meant that the economy was in a period of transition, which caused the high levels of unemployment without a ready supply of potential new jobs. I thought something similar was happening in Britain after the great financial crisis of 2007-2009 – and that this was the justification for the 2010 coalition government’s austerity policies (which were rejected by the left with religious fervour). The pre-crash economy had been too dependent on fake gains in financial services and related business services, meaning that it wasn’t just a case of managing aggregate demand, but allowing for a degree of restructuring, which takes longer. I don’t think anybody else made that argument. Supporters of austerity used versions of the household budget narrative, while most economists said that austerity was the wrong policy because aggregate demand was weak. I still think I was right – though by 2015 the case for further austerity had largely gone, meaning that further cuts made by the Conservative government from that year were excessive.

A final critique of the household budget narrative is made most prominently by advocates of Modern Monetary Theory (MMT). They point out that where countries control their own money supply (which is the case for Britain and America, though not the Eurozone), then they don’t need to worry about the national debt, because they can just create the money to fund it. This, in fact, is exactly what many governments did during the period of Quantitive Easing (QE) in the 2010s. For some reason, MMT is regarded as heterodox economics, and its advocates akin to heretics by conventional economists. I have never entirely understood this – it has always seemed to be a matter of politics rather than substance. Some MMT advocates delight in attacking orthodox economics, not always with secure logic, and this no doubt creates a backlash. Nevertheless MMT economists such as Stephanie Kelton produce well-argued work which is thought-provoking in a good way (this article in the FT gives a flavour). The central proposition is that the limiting factor for fiscal policy is inflation, not debt. While inflation in the developed world appeared dead and buried in the 2010s, MMT became popular on the left, as it suggested that large budget deficits were sustainable, supporting their argument that austerity policies were primarily “ideological”. In the 2020s, with inflation back in the picture, we don’t hear so much about MMT, though their analysis remains just as valid. My personal scepticism of MMT is that its advocates don’t tend to think enough about the difficulties of managing a small open economy, which has to manage its economic relations with other economies (and exchange rate policy in particular) – a situation that fits the British economy more than the American one.

What all these insights point to that there are two important constraints to fiscal policy rather than simply whether there is enough money: inflation and foreign debt (if we accept the MMT argument that domestic debt isn’t a problem if inflation is under control). Low inflation is central to a country’s feeling of economic wellbeing. I would suggest that maintaining the value of the currency is one of the sacred duties of the state – and governments play fast and loose with this at their peril – though most liberal economists are more relaxed about this. And foreign debt can interfere badly with a sense of national sovereignty. The reason that the recent left-wing Mexican president Manuel Lopez Obrador was so keen on limiting government expenditure was exactly that: a fear of foreign debt (and an example of how austerity is not always a matter of right wing ideology). Where governments have dormant inflation and little need for foreign debt (through a current account surplus), then budget deficits can run wild – this is the case with Japan, for example. In Britain things are considerably trickier. The country now has an inflation problem, and a long persistent current account deficit, which complicates managing the national debt. It is hard to know how much of a constraint the latter problem actually is. It hasn’t been tested to destruction since the 1970s (if you discount the Truss episode), when the government called in the IMF, though some suggest this was just political theatre. The country has had no trouble in financing itself from abroad in its own currency. The country’s dependence “on the kindness of strangers” is a popular scare story put up by officials of the Treasury and the Bank of England to keep politicians in their place. And yet, like inflation in the early 2020s, you don’t know if you’ve gone over the limit until it’s too late. It was a debt problem that did for Ms Truss’s bid for freedom, after all. That was a dislocation in the domestic debt market because of some technical issues with pension fund financing. I have oversimplified things by referring to “foreign” debt – but the presence of foreign investors affects the disciplines required across the whole market. That episode showed that management of the national debt has to be strategic – it is not a simple matter of ramping up a budget deficit and seeing what happens.

Meanwhile, I suspect that inflation in Britain remains a serious problem, in spite of the headline rate returning to 2%. In the public sector the government is no longer able to resist above-inflation payrises: you can only defy the market for so long – this is a large part of Ms Reeves’s black hole. That may ripple through to the wider labour market, as the previous government feared. Meanwhile there is enormous political pressure to reduce levels of immigration – and it isn’t just politics: high rental and property prices, in part driven by immigration, is causing serious hardship, and disappointed expectations amongst younger people. Politicians talk of encouraging a high-wage high-productivity economy, not dependent on cheap immigrant labour, and it might be that the country is in transition to just such a destination. But all economic transitions involve bumpy rides, and inflation is often part of that journey. That matters because under the country’s current economic governance, the Bank of England will not reinstitute QE, and make government debt easier to swallow, when there is a threat of inflation. And while reforming economic governance might be a good idea, in the short term it would carry a heavy risk of the destabilisation of financial markets.

So, with a clear menace of inflation, and more difficult markets for government debt, the government is likely to have to raise taxes. And here politics has created a further problem. Easily the most effective taxes are Income Tax, National Insurance and Value Added Tax. These are effective because they have a large base, meaning that small percentage increases have a big impact, and because they have the most direct impact on aggregate demand, helping the management of inflation. And yet Labour has ruled out increasing these taxes (other than through the “stealth tax” of freezing tax-free allowances). There was, in fact, a political consensus on that policy: no party is suggesting that there should be any increases – which is seen to add hardship to those already suffering from higher inflation. That leaves various flavours of capital taxes or wealth taxes. These have the political advantage of primarily affecting the better off, but they help with the national debt rather than inflation – their impact on demand is limited. And they are often evaded by people with tax advisers. That is the big problem with the idea, popular on the left, that increased state spending can be financed just by taxing the rich – such a policy would be inflationary and likely to underperform its targets.

Something has to give. The government will struggle on with continued austerity and increasing some fringe taxes, hoping for a growth bump. But growth is bound to disappoint, inflation will refuse to die, and interest rates will remain uncomfortably high. One commentator has written that it will not be until a second term that Labour will start to seriously address how the country manages the state – through some combination of higher (and doubtless reformed) taxes and reduced state ambition. If the Conservatives remain in a mess, that may become politically feasible. Up until now Sir Keir Starmer’s aim has been to secure an election victory, and to impose a more serious style of political governance. That is a start but it is not enough.

What do British Prime Ministers Sir Keir Starmer and Liz Truss have in common? The Labour leader defines himself as a complete contrast to his disastrous predecessor but one. But both made economic growth central to their political programmes. If that leads to a focus on economic efficiency, then this is doubtless a good thing. But the truth is that we are keen on growth as a way of avoiding hard choices.

Recently, writing in the Financial Times, the Oxford economist Daniel Susskind pointed out that economic growth has become the universal panacea for politicians, but that the political focus on it is comparatively recent. Indeed I think the political focus on growth statistics, including in the BBC news, is overdone. The voting public does not pay much attention to the statistical updates. The balance between income and expenses, the ability of governments to fund public services and welfare, and the state of the job market – these impact much more directly on peoples’ lives. All of these are supposed to be driven by growth, and yet the relationship is complicated. Nevertheless growth drives so much of the conversation amongst political elites that we need to ponder it.

But, as Mr Susskind points out, economic growth is poorly understood. Growth emerges from the actions of millions of individuals all working to their own priorities. Attempts to drive economic development (much the same thing, but with a longer history of political focus) by government fiat has led to some of the worst man-made disasters in history. Mao Zedong’s policy of collectivisation and the “Great Leap Forward” in China in the 1950s led to the biggest mass starvation event in history, followed by utter stagnation. Conversely Deng Xiaoping’s reversal of Mao’s policies in 1978 led to the most astonishing and important period of economic growth and development in world history. The simple act of letting farmers grow what they wanted and sell their produce on the open market boosted food production several times over.

Attempts to understand growth and develop policy have tended to focus on the supply side of the economy. That includes Mr Susskind – who homes in on innovation, which improves productivity. Sir Keir talks of investment doing much the same thing, and also the creation of more houses to allow people to move where the jobs are (or at least I think that’s a large part of why he includes housing in his growth agenda – although in truth he has shown little evidence of a grasp of economic policy). Ms Truss’s idea was to reduce taxes to provide businesses and workers with greater incentives to work harder.

But this misses something: the demand side matters too. There’s no point in producing more products or services if people don’t want to consume them. Mao’s strategy in the Great Leap Forward was to produce more iron in village smelters – but there was little use for the poor-quality metal that resulted. There is an underlying assumption that people will always consume more if they can – they are simply limited by the income they can earn from working. Of course economists know things aren’t as simple as this. People with higher incomes tend to spend a lower proportion of their income (leading to the rather more complicated question about saving, investment and growth). People may choose leisure, such as early retirement, which limits the supply of labour and often restrains demand.

And then, when you think about it, things get more complicated still. Once people have enough money to meet their basic needs, they often want to spend the surplus to signal social status. By and large this is done by buying things that are not made efficiently (hand-stitched bags, etc.) or services that require prodigious amounts of labour (personal trainers rather than fitness classes), reducing economic efficiency.

And then what about sustainability? Intensive farming delights economists because it maximises productivity. But it kills the soil, making it harder and harder to use it to produce anything of worth – and requiring ever more inputs of fertilisers, etc, which in turn create further environmental damage.

A further complicating factor is that the growth of the information economy means that the relationship between demand and supply is more complicated. Demand for information (including such things as music and video entertainment) can be met with little impact on production.

All of this raises two questions. The most obvious is whether growth is actually such a good thing. This is the basis of Green scepticism of growth. People’s basic needs must be met, of course, but beyond this we need to think about quality of life and sustainability. There are plenty of people whose basic needs aren’t being met, even in advanced economies like Britain’s – but dealing with poverty looks to be much more a problem of income distribution than the aggregate income across society. The United States has the largest income per head of any major economy – and yet strikingly high levels of poverty too. But economic efficiency is a good thing, provided proper account is taken of “externalities” (environmental damage, etc.). In principle it gives people more choices over their lives. Inasmuch as growth is simply our society becoming more economically efficient, then it is a good thing. If it destroys the planet or merely speeds up a treadmill of drudgery and pointless competition, then not so much.

The second question is more interesting. What if people, through the revealed preferences of their freely-made choices, don’t actually want growth? Growth is a popular idea, provided somebody else does all the work. But perhaps you would just like a nice place in the country and watch the world go by, rather than set your sights on ever more possessions or a frenetic succession of “experiences”. Growth, or the potential for it, emerges from the zeitgeist. In 1978 China, with so many people on the edge of starvation, it is easy to see why this zeitgeist was massively positive for growth. But in 2020s Britain?

Actually in 2024 Britain there are signs of a positive zeitgeist for growth – as many people complain about the cost of living. Sir Keir’s government may well be fortunate for a year or two. But the zeitgeist could turn – and we’d be back to swimming in treacle. And that would pose awkward questions for the sustainability of public services and the social safety net. Politicians and the public need to be focusing on these hard questions, and not just hoping that the growth genie will make them go away.

Back in the 1970s there was a persistent story about lightbulbs (then incandescent tungsten ones) that was trotted forth to demonstrate the madness of capitalism. It was that the life of a bulb was kept deliberately short so as to create demand for replacement bulbs. Apparently it was true – but nobody cared. Whinge as we might at the fringes, politicians and the public were happy to keep the economic treadmill going. Longer-lasting lightbulbs would mean fewer jobs. Those days are long gone. Our lightbulbs now are immeasurably more efficient, and they aren’t built to self-destruct. Few jobs are at stake, and even fewer jobs in countries that use the bulbs. This leaves the world materially much better off. But politicians and economists alike hanker after the those old days – hence their obsession with economic growth.

Even serious economic commentators like the Financial Times’s Martin Wolf can’t break this: Mr Wolf started a recent column with the words: “If the UK’s real gross domestic product per head had continued on its 1955-2008 path, it would now be 39 per cent higher.” This implies that the lack of economic growth in the last 15 years is a failure of economic policy, and not due to a change in the way the modern economy works. This is wrong: instead we should think of the second half of the 20th Century as a unique period in economic history – and recognise that we have long since entered a new era, one in which sustained growth of gross domestic product per head is not a feature – nor even really desirable. Life can get better, but not through consuming ever more stuff.

Economists don’t like to look behind their beloved aggregated economic statistics, which they like to treat as classical physicists once did the measurements of pressure, temperature and volume of gases. What the gas molecules were made of didn’t matter. Some economists try to construct historical time series of centuries and more in an attempt to build a narrative of economic policy, as if to say that there are common economic principles that are everlasting. To them the post-war era in the developed world, and parts of the developing one, featuring consistent growth is a model of wise policy. Firstly through good macro-economic management, with Keynesian demand management, and then inflation targeting monetary policy: these smoothed out the dips and troughs that were a feature of previous eras. Then there was a consistent advance of productivity through the use of new technologies and more advanced management. “Productivity is not everything,” said the economist Paul Krugman, “but in the long run it is almost everything.”

But looking back on it, that golden age was the result of the convergence of four factors, each of which has reached its limit: the post-war baby boom, bringing women into the workforce, the expansion of world trade, and the rising consumption of manufactured goods. The baby boom expanded the proportion of the workforce that was of working age, but by the 1980s the babies were now all of working age while the birth rate had fallen; and as the boomers reached retirement age in the 2000s, the proportion of people of working age shrank. The economist Dietrich Vollrath did the maths and found that this accounted for most of the tail-off of economic growth per head in the 2000s in America – and in Britain the effect would have been greater, if anything. This led to my comment that “Demographics is not everything, but it is almost everything.” The war brought many women into the workforce, but in the 1950s the convention that married women should stay at home remained powerful. But as families wanted to spend more on consumer goods and property (and technology made housework easier), women were steadily brought into the workforce, increasing the overall rate of employment, and thus driving growth. This trend has been slow but steady – the proportion of women at work was still growing through the 2000s – but now there is not a big difference between male and female employment, and in most economies, including Britain’s, the limit has surely been reached.

Freedom of trade has also been an important driver of economic growth, as the laws of comparative advantage and economies of scale came into play – in notable contrast to the pre-war years. First came GATT – the General Agreement on Tariffs and Trade, part of the great post-war settlement. Then, for Britain, there was membership of the European Economic Community – which in turn was given a major lift when this morphed into the European Union with its Single Market. But perhaps even more significant was the steady rise in Asian economies, and the huge increase in trade in manufactured goods – a succession starting with Japan, moving through to the Asian “Tigers” (Taiwan, South Korea and so on) onto China, with India in a supporting role. The rise of this trade, referred to as “globalisation” was transformative. The cost of manufactured consumer goods in the early 2000s tumbled as a result, and was one of the critical underpinnings of economic growth. But this trade is no longer growing – and is probably shrinking, while Britain has left the EU and Single Market. Gains from trade are unravelling. This is partly a product of the rise of protectionist politics, but it is also because economic convergence has reduced the potential gains from comparative advantage. Funnily enough the reversal of globalisation is often celebrated by politicians, almost in the same breath as they call for stronger economic growth.

These three factors are well-known amongst economists, even if they don’t talk about them enough when considering the slowdown of economic growth – compared to familiar targets such as lack of public and private investment, NIMBYism, muddled political policy and so on. In contrast my fourth factor seems to be less well understood. In the post war era there was a massive expansion of consumer goods, from cars to cosmetics. This was made possible by advances in technology during the war, with the development of plastics, for example. Keynesian economic policy helped to pump-prime a virtuous circle of increased supply and demand – the expansion of manufacturing and distribution jobs helping to fuel demand. This cycle became central to the growth of advanced economies, copied by many less developed economies, though, interestingly enough, not so much by China, which is another story (they channeled much more of the extra demand into investment, relying on exports much more for growth). Along the way absurdities like the built-in obsolescence of light bulbs were tolerated. Many view this era, up to the late 1970s in Britain, as something of a golden age: one with a largely stable working-class culture, geographically well-spread, and quite a bit of upward mobility into an expanding middle class – before the destruction of the industrial heartlands that started in the 1980s. This view requires rose-tinted spectacles. Some things were clearly better then: access to social housing, for example; and this, combined with high taxes on the rich meant lower inequality and better social cohesion (so long as you weren’t brown or black skinned). Public services were more generously staffed, though usually terribly managed. But was an era of massive environmental degradation and plenty of social strife; film and television dramas of the era depict people shouting at each other but failing to communicate – which is largely how I remember it as I was growing up.

But this age of expanding consumerism could not be sustained. There are only a certain number of cars, fridges and so on the people can own. There was a limit to the amount of electric light that people could constructively use. And besides, advancing productivity meant that fewer jobs were required to sustain demand, and expanding trade kept up fierce pressure on efficiency. The final blow came when when, for reasons of comparative advantage rather than efficiency, the developing economies of Asia took over a huge share of the production of consumer goods. The 1980s onwards saw massive closures of factories and other infrastructure, such as coal mines.

But the standard rejoinder to this from economists is that these developments shouldn’t really matter. Cheaper consumer goods mean that people have more to spend on other things, and these require people to provide them – and these people can be made more productive. Lightbulbs may have been replaced by cheap LEDs made in China, but the new technology can be arranged into much more complicated and creative arrays, which need people to design and install them. But there have proved to be a number of problems with this idea. Economists will admit that manufactured consumer goods have largely been replaced in the modern economy by services, where productivity is a much trickier thing. They call it “Baumol’s Cost Disease”, teach it in Economics Batchelor degrees, and then forget about it.

Unfortunately, a Batchelor Economics degree is as far as my formal economics training went. The theoretical complexities of an economy where increasing productivity comes about through higher quality rather than quantity, and were an increasing amount of consumption goes into access to land, rapidly takes me out of my depth. But the outcome of these complexities is surely that developed economies do not behave as they once did. One problem is that the modern economy is more unequal. Large numbers of people are now extremely well off by past standards, and we have the phenomenon of “mass affluence”. Millionaires are commonplace. But at the other end of the scale many working class jobs are much less secure than the factory and office jobs of the past. The better-off, meanwhile, spend a lot of their money is on status goods and services, rather than basics. (They also save more, which complicates things more – though overall savings rates have gone down rather than up). One of the key ingredients is human content. In olden times this might be the number of servants you employed; nowadays it is the consumption of personal services and use of products whose whole point is that their production processes are inefficient (hand-stitched handbags, etc.). These often require low-paid people to provide. There is surely a danger that this inequality gets entrenched, and that this is a drag on economic development. This is surely one reason that minimum wage policies have not caused the damage that a consensus of economists predicted in the 1990s.

Then you have the problem of leisure. One way for people to exploit the benefits of higher productivity is to work less. This might be more holidays, or (as in my own case) retiring early. Then there is the hobby economy – where people produce things deliberately on a non-commercial basis for the sheer enjoyment of it. All this is perfectly rational economically, but it makes a mess of classical economic assumptions. And here’s the thing: a society were people don’t have to work as hard to achieve a comfortable and fulfilling life is not a failure. But listening to conventional economists you might think it was. Such a society is taking shape through the freely made decisions of economic agents: it is not a failure of policy. We need to understand how much slow growth is the result humanity realising the benefits of greater economic efficiency, and how much is through dysfunction – and I will admit there still quite a bit of dysfunction about.

So what are my conclusions? Firstly it is that most economists are suffering from a fallacy of composition when talking about productivity and growth. They have a mental model of the supply side of an economy being a single business scaled up (“UK plc”) when the reality is much more complicated. Advances in productivity in one place can simply lead to a reduction somewhere else. Secondly we are often confusing the creation of wealth with its realisation. Many people rationally choose to realise wealth by earning less – and the number is growing. Thirdly, the inequalities in our economy aren’t just a bit of untidiness that will resolve itself, but need to be a central focus of economic thought and policy development – as this is likely to do more to advance economic wellbeing that overall economic growth.

Politically this means that both the left and the right are barking up the wrong tree – at least as represented in Britain by the Labour and Conservative parties. Conservatives hanker after a low-tax high-growth society, powered by free-wheeling entrepreneurs. Those days are long gone. Lower taxes simply increase inequality and have nothing to do with growth. Labour assume that better direction from government towards constructive investment will unleash growth that will generate taxes that will fund improvements to public services. This is a lot less wrong-headed than the Conservative narrative. After the years of chaotic Conservative government, it is surely true that a bit of grown up government will unleash a some catch-up growth, enough to generate a bit more tax revenue – and maybe even to lift growth to the top of the G7, as Labour predicts (doubtless thinking that the other six economies are due for a bit of a stall…). But it can’t last – and the party is not ready for the hard choices that lie when it all fizzles out and they are forced to confront various combinations of austerity and higher taxes.

What we need to do is to take a fresh look at society and its dysfunctions and address that dysfunction through slimmer but more effective public services, and intelligent redistribution. Technological advance continues to offer the opportunity to advance human wellbeing – but we will get there faster if break the growth mindset.

I asked Bing Image Creator to give me a picture of shoppers in an English town buying foreign goods. This is one of the four results. Me neither.

Somewhere over the Christmas holiday I heard on BBC Radio 4 a very authoritative gentleman suggesting that Britain should copy Japan’s economic policies. Alas I didn’t catch who it was, and can’t trace him. I think he was on the World at One, but these days the BBC doesn’t let you search past programmes for particular items. Anyway, it is an excellent illustration of the point that I was making about the British economy a couple of posts ago. It’s worth explaining why he is so wrong. I suspected that the gentleman was a graduate of PPE at Oxford, like former Prime Minister Liz Truss: a degree course that equips its subjects to sound plausible when talking about economic policy, without necessarily grasping even the basics of the subject. Ms Truss did not seem to realise that reducing inflation meant limiting demand.

The particular set of Japanese policies the interviewee referred to dates from a number of years back, and was advocated by the late Japanese Prime Minister Shinzo Abe, and is often referred to as Abenomics. He himself called his approach as the “three arrows”. This was based on the ancient wisdom that while it is easy to break the shaft of a single arrow, it is hard to break the shafts of three arrows bound together. His three arrows were monetary policy (ultra low interest rates supported by Quantitive Easing (QE), i.e. the buying of government bonds by the central bank), fiscal policy (extensive infrastructure investment funded by budget deficits) and supply-side reforms. All these policies were mutually reinforcing. Supply side reforms were required to expand the capacity of the economy, fiscal policy to ensure that aggregate demand met this this expanded capacity, while loose monetary policy made the large government budget deficits implied by this sustainable. Without all three strands of policy, there would be failure. Japan had endured many years of economic stagnation, and Abenomics was an elegant and coherent approach to this – more than can be said for British policy economic policy since 2010, when the different policy levers often seemed to work against each other.

The interviewee did advocate one point of departure from Abenomics. When explaining supply side reforms, he advocated three “Is”. The first of these was “investment” – I can’t remember what the other two were (perhaps “institutions” was another). Investment was not a focus of Abenomics. Fiscal policy was directed at public investment, admittedly, but there was little economic coherence to this – it. was mostly about the dispensation of political favours (“bridges to nowhere”) – and the desired economic impact was to raise aggregate demand, not to expand economic capacity. Supply side reforms were aimed at non-financial barriers that were holding the economy back, such as the low rate of employment of women, and not investment.

So what’s wrong with all this in the British context, skating over its mediocre results in Japan itself? Japan was, and is, in a very different economic place. It has a robust industrial base which routinely delivers export surpluses, in spite of having to import raw materials and energy. It has a high rate of domestic savings (in other words domestic consumption is much less than income). Investment is plentiful. But it has all manner of market inefficiencies due to conservative business practices and cultural mores (for example severe prejudice against working women). Contrast this with Britain: its industrial base is comparatively weak, delivering no trade surplus so far this century; the private savings rate is low; investment is weak; but business practices, regulations and social mores are as conducive to economic efficiency as they are anywhere in the world – with a high rate of overall employment, for example. Both countries share grim demographic trends, with a reducing ratio of people of working age – though Britain has been mitigating this with immigration on a scale that Japan doesn’t.

What ails Britain? Pretty much everybody seems to agree that the country lags other developed countries, though whether you compare with America or with Europe depends on your politics. Apart from the lacklustre growth record since 2007, the main evidence is poor comparative statistics on productivity. A lot of the analysis is very shallow, however. Even many academic economists who should know better are susceptible to the fallacy of composition. While they quickly recognise that national decisions on budgeting and demand management are not the sum of individual household budgets – and what would be right for a household would not be right for the country as a whole – they fail to see the same thing on the supply side. They often talk of the country’s production side as if it is a single business (“UK plc”), but that is grossly misleading.

For a start, the supply side of the economy is very heterogeneous. Computer factories are highly productive; hospitals are the opposite. It doesn’t follow that we would be better off if we closed our hospitals and replaced them with computer factories. Furthermore, if individual businesses become more efficient, it also does not follow that this translates into the whole economy doing so. That depends on what those individual businesses do with their extra efficiency. They might expand production, perhaps helping to expand the economy as a whole – provided that there is latent demand for their product. If this happens there may be a virtuous circle that helps the whole economy grow. Or they might just keep production levels steady and sack some workers, paying extra dividends to investors who use it to invest in other businesses. Or the directors may pay themselves more in bonuses to spend on personal trainers, luxury goods, and other things where low productivity is the essence. Overall there is a well-established pattern, however, referred to by economists as the Baumol effect. As productivity advances in some sectors of the economy, lower productivity industries come to occupy a higher proportion of the economy as a whole. The balance of wealth creation (highly productive industry) to wealth realisation (the part of the economy that prioritises self-actualisation and typically has a high human content – i.e. low productivity) shifts towards the latter. What’s the point of being rich if you can’t access decent healthcare, drive around in Bentleys or eat organic food?

The problem for Britain is that the overall mix of its economy is out of kilter. It imports a disproportionate share of the goods and services where productivity is very high, while producing too much of the goods and (mainly) services that are critical to quality of life, but where productivity is low, and export potential is much weaker. The answer isn’t to try and raise the productivity of the latter goods, as this will tend to kill the quality. It into rebalance the production side of the economy towards high productivity goods that can be exported. There is another way of looking at this problem: it is that British consumption is too high. We are living beyond our means, importing more than we export. Consuming less would give the supply side of the economy the chance to rebalance in favour of exports. This is the opposite problem to Japan, where aggregate demand tends to be too low for economic efficiency. In Britain there needs be more private saving and more investment. In Japan it is the opposite.

So Abenomics would not work here. Looser fiscal policy would push us into inflation. Loose monetary policy would simply build speculative bubbles. Supply side reform would not make enough difference, though doubtless there are some useful things to do.

But the interviewee was right about one thing: the key to progress in Britain is greatly increased investment. Any move to highly productive, high exporting businesses will entail substantial investment. What are these businesses? Basic economics teaches us that these should focus on areas where the country has a comparative advantage – but that is a very slippery thing to identify. We shouldn’t be chasing a past golden age, or trying to directly copy other successful economies. If you care to look, there are areas of promise – for example life sciences, especially if the country can tap into NHS patient data. The government, at least does seem to appreciate this – it talks about building the industries of the future. But it struggles to deliver the right economic conditions to generate the level of investment required. There are not enough private savings to fund the business investment required; too much of what there is disappears into government debt – pushed that way by conservative regulation.

This points to a different three arrows to those advocated by Mr Abe. We need to incentivise more equity investment in businesses with export potential – especially if these are based outside London and the South East. Much of this must be led locally by regional and local governments, able to raise their own revenues. Pension regulations need to be overhauled. Second we need a much tighter fiscal policy in order to damp down private demand and keep inflation in check – this will consist of higher taxes and more efficient government (e.g. coherent public services that solve problems rather than passing the buck). If the public won’t save more of their own volition, then the enforced saving of higher taxes has to do the job. This would then give the government space to kick-start investment and tackle bottlenecks. Third monetary policy should primarily be focused on creating a healthy climate for savers, and ensuring financial stability. That will surely mean higher interest rates.

No politicians can advocate steps two and three of this programme. But the first part is near political consensus – and we could find that it drags fiscal and monetary policy in its wake. British policy usually advances by muddle. It is possible that the country will muddle along in the right direction. That is the best we can hope for.

In my last post but one I discussed how Britain’s politicians are in denial over the hard choices that need to be made over taxation – evidenced by a fatuous Autumn Financial Statement from the Chancellor of the Exchequer, and the inadequate opposition response. Now The Resolution Foundation has published a new report: Ending Stagnation: a New Economic Strategy for Britain, based on a substantial amount of research, and again we are coming back to the growth problem.

Unfortunately I haven’t read this worthy and weighty contribution to the debate. It is nearly 300 pages long and describes itself as a “book”. Instead I have read the Executive Summary and some of the commentary, including from Torsten Bell, the Resolution Foundation’s Chief Executive, amongst other reviews. These leave me a bit confused, and clearly a lot of the devil (and perhaps some angels too) is in the detail. Given my substantial reading list, getting round to reading the detail will take some time.

Mr Bell has been trying to paint an optimistic picture – that Britain has the opportunity for catch up growth based on its weak performance: something that I have mentioned, amid my rather dismal assessment of longer term growth prospects. He points to two opportunities in particular: strengths in service industries which can be an engine of export growth, and the ability of Britain’s weaker regions to narrow the gap with the prosperous London and South East.

The point about services is an interesting one. It flows from two propositions that I agree with. The first is that manufacturing is yesterday’s story; it has become so efficient that there are few jobs in it, and besides there are saturation effects as the link between consuming quantities of stuff and improving wellbeing weakens. The second is that export industries are critical to most models of economic growth. Most successful economies in Europe and the developing world run trade surpluses. The US is an exception, but it is also an export powerhouse – it is just an import powerhouse too. The position of the US in the global economy is unique, however, and it doesn’t offer Britain any kind of hopeful model.

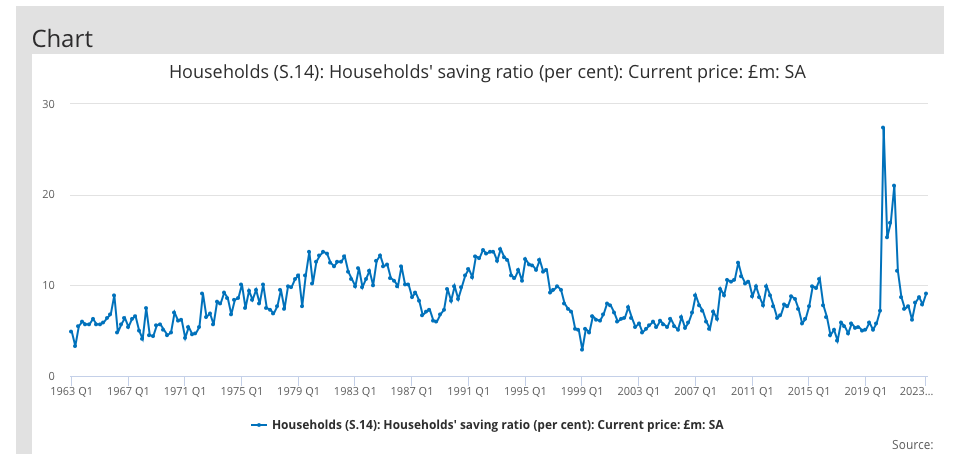

Why should exports be so important? That is a bit harder to answer. The explanation often advanced is that export industries are usually highly efficient (especially if they are not about mining and natural resources), partly because they have to be globally competitive, and partly, doubtless, because supplying things across borders requires a degree of efficiency anyway. There is doubtless a lot of truth to this. And this is linked to another truth, which is that exports and investment go together. This is in turn is linked to basic macroeconomic dynamics. A country with an export surplus consumes less than it earns – otherwise all the exports would be balanced by imports. And that usually means that such a country has high investment levels, as that surplus needs to be spent somewhere. That oversimplifies things quite a bit, of course, and disentangling cause and effect can be hard. But if Britain is going to play the catch-up game I am sure that it means three things that are very closely linked: better balanced trade (currently there is a 2.9% current account deficit – one of the largest amongst bigger economies, though America’s is close at 2.8%); greater levels of investment; and a higher rate of personal saving (currently 9.1%, actually relatively high compared to the pre-covid period, but still much lower than the EU average of 18.2%).

The first two parts of this trilogy are uncontroversial. Pretty much any commentary you care to read on the UK economy mentions the need for more investment, both private and public. People are less explicit about the need for more balanced trade. Back in the 1960s and early 1970s, before floating exchange rates and free capital flows, this used to be a matter of high political drama. Since then it has dropped from the conversation; Britain seemed to be doing just fine in spite of regular and large negative balances. But conversations about growth often turn to greater export volumes, and that implies more balanced trade. But surely something else is true: the country needs to import less if it is to save more and provide the funds for investment. And that means consuming less. There is a strikingly similar conversation to be had about tax. Higher public investment, and better quality public services, and a more adequate social safety net, imply higher taxes… and less consumption.

Looking at the graph of Britain’s savings rate over the last 70 years (above) it is hard not to see the supposedly economic golden years of new Labour, from about 2000 to the crisis of 2007-09, as a bit hollow: a consumption boom based on reduced savings levels. It was linked to a consistent current account deficit (the last surplus was in the mid-1990s). I have always thought this economic achievement was less than it appeared, driven as much of it was by the spurious profitability of the banking sector, which was reversed in the financial crisis. One important aspect of the decline of personal savings in this period was the reduction of corporate pension schemes. I witnessed this at first hand as a finance director in the first part of the 2000s, with presentations from consultants offering to reduce the costs and risks of pension schemes for employees. Final salary schemes were replaced with money-purchase ones, which almost always entailed a simultaneous reduction in contribution rates. This was sold as an advance for personal autonomy over the patronising ways of the past. In truth the potential liabilities associated with final salary schemes, or more correctly defined-benefit ones, were quite scary, and they gave employees who changed jobs a rough ride. Also the general decline in interest rates made those promises more expensive to keep. But now the collapse in pension funds as the source of UK business investment is much remarked on, though people tend to blame the post-crash flight to safety in pensions regulation; its roots are much deeper. Attempts to revive domestic business investment by the Chancellor look puny by comparison with the larger economic forces in play.

How might the savings rate be increased? The best way surely is for the current rise in interest rates to be sustained. This will deliver higher returns on new savings, even as it damages the capital value of past savings. There is a paradox here. It is often claimed that lower interest rates are required to stimulate business investment, but reducing the costs of finance. But the finance director in me says that cheap finance means poor-quality investment. There is nothing like a higher target rate for return on investment to focus minds on the best way to structure an investment project. I have seen it time and again.

Another problem with higher interest rates is that, all other things equal, it will drive up the exchange rate. This would make exports more expensive and imports cheaper – working against reducing the trade deficit. it would tend to make the country less attractive for foreign business investors. But part of the attraction of raising domestic savings is that it reduces the dependence on foreign capital, which is less reliable for a medium-sized economy like Britain’s. Many of Britain’s most successful businesses are foreign-owned and based on foreign investment. And yet, in spite of a relatively cheap pound, these foreigners have not invested much recently, especially since Brexit.

Unfortunately there is no guarantee that higher domestic savings would lead to more productive business investment. The old defined benefit pensions were a particularly effective channel for this purpose, and they are gone for good. More money could be pushed into domestic property – though some funding for this sector would be a good thing, so long as it just isn’t a matter pushing up land prices. Funds could be swept up by government debt, if budget deficits are not also brought under control. But buy and large a higher interest rate environment is more conducive to productive investment, rather than fuelling speculation. High interest rates are not good for the property market, which in current conditions is a good thing. Serious thought needs to be given to pension reform so that there is greater level of collective investment – as this is most likely to be channelled productively. There are examples from other countries of ways that this might be done (the Netherlands and Australia come to mind).

So my recipe for getting the British economy onto a healthier path includes higher taxes and higher interest rates. This is not going to be taken up by any political party – but parties in government might be forced into that route anyway. The Conservatives seem the least likely to do so – with their agenda of tax cuts and supporting property prices. My favoured option is for a Labour-Lib Dem coalition – which would require a hung parliament, and both parties having the stomach for a coalition. On present evidence neither proposition is looking likely. A large part of Britain’s lacklustre performance comes down to our prioritisation of personal consumption. Changing that is a hard road.

This week’s Autumn Statement by Britain’s Chancellor of the Exchequer, Jeremy Hunt, was a miserable affair, full of political chicanery with little to effort to tackle the country’s deepening problems. Worse yet, the opposition parties (Labour and the Lib Dems anyway), for all their huffing and puffing, are also unable to face up to these problems.

The Conservatives billed the set of measures as the biggest set of tax cuts since the 1980s. And yet the overall tax burden is rising as the freezing of tax allowances and thresholds will bring ever more people into tax or higher rates of tax, and increase the proportion of income people pay as tax. An even bigger problem is that the government has been using inflation to squeeze public spending, while services across the board – health, education, the police, the courts, and the list goes on – are clearly overstretched and in many cases breaking down – with collapsing buildings and rising waiting lists. The Chancellor offered not a penny to alleviate this crisis, while planning a further squeeze in the years ahead. Labour and the Lib Dems gleefully pointed out the first problem, but failed to address the second. They will stand by the announced tax cuts, while offering only gestures (taxing non-domiciled residents, or private schools, for example) to help fund public services. These tax-raising wheezes are nowhere near enough to match the scale of the crisis. Meanwhile all parties suggest that a bonanza of economic growth is coming to the rescue, without acknowledging the severe headwinds that will limit the country’s long-term growth prospects.

I am also highly sceptical of the one measure that seems to be getting widespread support – the full expensing of investment in machinery and systems against corporate profits. It is said that this will boost business investment, which is sorely lacking. It is in a fact the revival of a policy that failed in the 1980s, and was abolished by Nigel Lawson, the Tory tax-cutting Chancellor, who has been about the only holder of that post in memory that had a grasp of how the tax system as a whole worked and could be reformed. Back then it created a tax-avoidance industry and encouraged wasteful investment with fancy kit, rather than the thinking through of business processes which is the real key to improved productivity. That fiasco occurred at the beginning of my professional career as a Chartered Accountant, where I could see the nonsense it was creating up close. Alas the current crop of politicians and their advisers are too young to remember this. And it is of little use to new businesses, where the need is most acute, as these typically do not generate enough profit for this to be of use. What a silly waste!

Meanwhile the fiscal climate is getting a lot worse. Interest rates are rising at time that the size of the national debt is historically very high. If interest rates are higher than the overall rate of growth, and there is a budget deficit, then a debt spiral threatens, which, if it leads to an international loss of confidence in the public finances, could usher in a severe financial crisis. At the moment it is actually quite hard to understand how much of a problem this is. You should be comparing real interest rates to real growth rates – i.e. after inflation. But there are mixed signals on real interest rates. If you compare the nominal rate on government lending, it is if anything less than reported inflation – indicating a negative rate. But yields of index-lined bonds are positive and have risen sharply. Meanwhile the budget deficit is quite high – at 4% of GDP. It wasn’t so long a go when none of this seemed to matter. Interest rates were low, and the Bank of England’s Quantative Easing (QE) programme made large government debt look manageable. But conditions have changed. Inflation has made money much tighter – with interest rates rising, and QE going into reverse. I am starting to suspect a deeper change is afoot in the world’s capital markets. Earlier this century a number of countries ran large trade surpluses – notably China, Japan and Germany. This made trade and budget deficits more stable in countries like the UK and US, as the surplus countries had plenty of spare currency to provide funding. As the world’s trading environment is getting more difficult, this may changing – though it is not yet evident in public statistics. After over-reacting to fiscal risks in 2010, and moving into austerity too quickly, the opposite risk beckons. But the Autumn statement proposes tackling the budget deficit only slowly, leaving the very high level of net debt virtually unchanged. Politicians seem to assume that as inflation comes down things will simply go back to the easy financial environment that pertained before. This is complacent.

More from the OBR report – government plans make little impact on public debt

If that is complacency, the politician’s attitude to economic growth is outright denial, though some economists who should know better seem to be in the same place. It is assumed that the UK’s poor performance has an easily fixable cause. More investment perhaps, or encouraging more people into work, or perhaps lower taxes. Rachel Reeves, Labour’s Shadow Chancellor, blithely talks about sorting out public services through economic growth – even applying the first-person to the process, as if growth was the gift one individual, and not the collective result of many millions of decisions. International comparisons seem to show that Britain’s productivity lags against peers. All that we need to do is fix this, the argument goes, and we will unlock growth. Well it may be that a burst of catch-up growth that is obtainable – but I suspect that these comparisons reflect an irreversible de-industrialisation, when a swathe of high-productivity industries left the country in the 1980s and 1990s and will not return. But stepping back, most or all of the developed world faces a number of headwinds that reduce growth potential, and in some case send it into reverse:

Demographics: more people are retiring as lower birth rates take their toll. Immigration can make up some of the difference, but is politically fraught, and stresses housing resources.

Trade: as globalisation runs into reverse, gains from trade are turned into losses. The UK is spared the American obsession with “near-shoring” or the reversal of the off-shoring of industries – but we have our own demons unleashed by Brexit.

Overdevelopment. The increasing consumption of goods, a critical driver of past growth, is simply a phase in economic evolution that has clearly ended. People move on to improve their quality of life in other ways. Meanwhile massive increases to the productivity of manufacturing industry mean that its impact on the total economy is much reduced. All this means that lower productivity parts of the economy, including many public services, loom larger. Productivity gains are harder to get, and where they happen the result is not so much increased production, but a transfer of resources to low-productivity sectors.

The energy transition. The country needs to make big investments to sources and distribution of energy, and its more efficient consumption. While the end result is desirable, in the meantime this will push down consumption. This, in fact, applies to pretty much all forms of investment. The country has become used to high consumption and low savings – reversing this won’t necessarily reduce growth as it usually measured, but to many people it will feel that way.

Housing. One way of achieving growth, or at least burst of catching up, is to allow people to move to places where the most productive jobs are. But these areas lack enough housing to accommodate this. Britain’s house builders have growth rich on the skilful management of land portfolios, rather than the actual building of houses, which many are actually very bad at. They have no incentive to increase the pace of building. And if the pace is increased, skill shortages quickly become evident. And I haven’t even mentioned slow and restrictive planning processes. Politicians at least show some awareness of this issue, but action never matches the promises.

The days of steady economic growth over the medium to long term are over, whether we like it or not. The best we can hope for is a short-term spurt. There is plenty of potential for human wellbeing to improve, but this will manifest itself in other ways.

The central problem is the funding of public services and maintenance of social safety-nets. A combination of two things are required here. The first is higher levels of taxation – and mainstream taxes which directly affect demand, and not gimmicks around capital and wealth (the latter may help make debt more manageable, but won’t suppress demand and prevent inflation). The second is a radical reform of public services so that demand for them is reduced – reducing the level of social problems, so that we require fewer police, courts, hospital beds, etc – and managing those problems so that they are solved early rather than passed from agency to agency. Alas we have very little idea how to bring such a change about – though we can see that some countries do this better than us (Japan, Switzerland, Denmark perhaps). A radical reform of government is clearly a part of this, with less centralised control – but it needs much more than this: decentralisation by itself could actually make things worse. With the possible exception of education (which has become more effective rather than cheaper) the reform efforts made by our governments in the last twenty years have taken us in the wrong direction – from Labour’s over-centralisation, to the de-skilling and outsourcing of the Conservative and coalition years. Unfortunately the choice between the two approaches of higher taxes or radical reform is not a binary one. Reform will require substantial investment, and that is likely to mean higher taxes in the short term at least.

If our politicians are in denial about all of this, how about the public? They surely understand that public services are in a dire state – and that fixing this will not come cheap. But they are too wrapped up in their own personal struggles to spend any energy on demands for change. Politicians are in denial for a reason: they don’t just a lack imagination and perception, but they also know a voter-loser when they see it. Still, Labour are clearly presenting a more realistic prospectus than the Conservatives, even if it is based on wishful thinking. Their poll lead at least seems to show some wider awareness by the public at large. And we must grasp at that straw.

I apologise for not posting for some time. Feelings of futility and despair at politics have made gardening and painting model soldiers a more attractive pastime. I started an article last week, but this collapsed in a muddle. This time I want to step back and set current debates over the political economy in the broader historical context – to suggest that we need to adjust our expectations to profound changes to the way economies work. Above all this means letting go of ideas about economic growth and all the baggage that goes with it. The implications for our politics are profound.

Economists sometimes like to portray their discipline as the description of immutable laws. They show tables of statistics (or rather graphs – see above) going back centuries – with uniform metrics such as income, prices and productivity. The idea is to present the economy as a continuum, even if as the world behind it changes. This might lead us to think that the tools of economic management are of timeless relevance. What if Keynesian demand management had been discovered earlier! But this is really an attempt to project the present back into history. The world has been changing profoundly over the last three centuries and the economy with it. With these changes come changes to our ideas of what economic management is about, and politics with it. But the process is slow and complex, and it can be hard to appreciate it at the time. That’s why I think it is helpful to paint a picture of how things have changed in the past, to give an idea about how things might be changing again now. I like to rationalise the past into a series of epochs – but, of course, each each moved seamlessly into the next. This narrative is based on how things were in Western Europe in particular, and by extension its colonies in North America.

The first epoch was the Age of Subsistence, from Medieval times into the 18th Century, which was overwhelmingly agricultural and marked by stasis. There were important technological developments, and the changes to trade patterns also had important impacts. Textiles, mining and iron working played a role, leading to occasional local booms and some nice stone buildings for us to see today. There was sufficient agricultural surplus to support a number of cities and towns. But the overall picture was fairly static and based on agriculture, mostly of a subsistence nature. The vast majority of people worked on the land in a very low-productivity agrarian economy. The big political idea was that people should know their station and not get beyond themselves. The idea of abolishing poverty was considered to be delusional nonsense. God created a world ever divided between the aristocratic rich and the peasant poor, and that was that.

Then came the Industrial Revolution, which was initially based on textiles and agriculture. Farming became more efficient, not so much directly from changes in technology, as from the application of scale economies, with enclosures and evictions. Agricultural surpluses could be moved by canal, and the cash economy expanded. Labour moved to textile mills, where mass production techniques were developed. Also at this time slave labour was used in overseas colonies to produce such products as sugar, tobacco and cotton. Trade grew in importance and a substantial middle class emerged. Social mobility became more of a feature of society. A lucky few managed to climb from working class to middle class; an even luckier minority of middle class people aspired to the aristocracy. But the labouring classes saw no improvement in their lot. There was no move to reduce poverty. But the new middle classes questioned the ways of the governing elites and this had a profound political impact – most notably be the American and French revolutions – but also with such things as the anti-slavery movement in Britain.

This moved, in the 19th century, to the Age of Heavy Industry. This saw the rise of railways and steel. Infrastructure (railways, ships and sewers for example) and armaments became the centre of attention. Right though until the middle of the 20th Century, economic success was measured in terms of the rise of heavy industry. Hermann Göring’s statement that “Guns will make use powerful; butter will make us fat,” summed up the way that most people thought about economic policy. Stalin’s building of Russian heavy industry at the cost of millions of lives was generally considered to be tough but rational. But improving the lot of the poorest did start to command political attention, as working class movements rose. Sanitation improved, free education was offered to all, and a welfare state started to emerge. This age culminated during the Second World War, which was largely decided by industrial production. But it quickly morphed into the Age of Light Industry. Many of the technological developments forged in the war, such as plastics, turned out to have applications in consumer products. And the need to switch away from war production offered the opportunity to greatly expand the production of mass market consumer goods. Pretty soon mass consumption was considered to be the top priority for the political economy. The concept of economic growth was developed to reflect this and the prospect of abolishing poverty. The West won the Cold War because the Soviet empire could not compete in the production of consumer products, and its leadership lost confidence in their raison d’être.

Something else profoundly important developed alongside the consumer economy: the rise in the role of the state. The state greatly expanded in wartime, intruding into all aspects of life. People noticed that rationing meant that austerity in the nation as a whole did not mean that the poor had to starve – indeed nutrition for the poorest improved in Britain. This vindicated a role for the state in providing a social safety net, with health insurance, unemployment pay, expanded pensions and so on. Productivity was high enough for agriculture and consumer goods that there was room for a growing state sector. Politics became managerial, with politicians promising to offer prosperity to all. Social mobility exploded.

But the world has moved on. Many noted a major change in political and economic thinking in the 1980s, following he economic travails of the 1970s. There was a push-back on the growth of the state and on organised labour. De-industrialisation started to take hold as productivity continued to advance in manufacturing. The rise of Asia, starting with Japan, offered gains from trade as cheaper manufactures could now be imported. But growth in consumption still dominated expectations. Manufacturing industry was still considered to be the core of the economy, much as agriculture would have been in the 18th Century.

To understand how things have changed, consider a few things about the world around us, in developed economies. First are the signs of saturation in consumer demand. Of course there are plenty of people struggling with the basic necessities – but they are a minority. Meanwhile people buy cars absurdly over-specified for their needs, and leave them parked outside their homes doing nothing most of the time. People buy clothes to wear once or twice before they are discarded. Much of people’s wealth is spent chasing things that are not made – notably land for homes, even if just for temporary residence rights. A lot of “consumption” is in fact about the acquisition of status symbols.

Then there is the idea that consumption is actually bad for us. Environmental degradation is one example; climate change is another. And then there is health. Highly processed foods, where agriculture and manufacturing meet, are clearly damaging to our health, and one reason that life expectancy is now in decline. And yet to economists they are ideal commodities: based on high productivity and promoting over-consumption, and thus with beneficial economic impacts. Better off people increasingly choose products that are healthier with reduced environmental impacts (though still prone to massive over-consumption) – but these imply reduced productivity – the biggest crime there is in the Age of Light Industry.