The Pantiles, Royal Tunbridge Wells – photo Paul Collins

Media commentary on British prime minister Rishi Sunak’s cabinet reshuffle largely misses the point – the exception being the FT’s Stephen Bush, whose newsletter came out after I started drafting this – and who is absolutely on point here. Most reflect on the ironies of the shock appointment ex-prime minister David Cameron to be Foreign Secretary, and the impact this may have on various groups of voters. Many cast it as the desperate act of a failing administration. I would rather see it as a rather brilliant move to the front foot.

First things first. The most important move yesterday was the removal of Suella Braverman as Home Secretary. She was never qualified for the job and, predictably, proved a loose cannon. But she is a darling of the Tory populist wing, who gave her a rapturous reception at the party conference – and her appointment was widely regarded as necessary for Mr Sunak to secure his uncontested nomination to the top job. Last week her attention-seeking criticism of the pro-Palestinian demonstrations and criticism of the police helped take the heat off Labour leader Sir Keir Starmer’s typically leaden response the Gaza crisis. This was an excellent opportunity for the Conservatives to cast doubt on Sir Keir’s ability to take on the job of prime minister. Instead the story was Ms Braverman’s extraordinary conduct – which included direct defiance of Mr Sunak in an article published in The Times. That undermined Mr Sunak’s authority. This exasperated respectable Tory-leaning voters in places like Tunbridge Wells, without doing much to rally disaffected voters in places like the West Midlands, site of a recent spectacular by election loss, which had been critical to the party’s success in 2019.

But by appointing Lord Cameron, as we must now call him, to the cabinet Mr Sunak relegated the Braverman story to the back pages. Instead of outrage by her supporters bringing attention to the fractured state of the Conservative Party, all anybody wanted to talk about was Lord Cameron and Mr Sunak stamping his mark on on the cabinet. Ms Braverman’s sacking was passed off with a shrug as a rather obvious move. She will try to regain the initiative – she is clearly politically ambitious – but it will be hard for her to recover. Her moment has passed. The Tory populists will seek out other standard bearers.

This will do much to reassure those voters of Tunbridge Wells, a short drive from where I live. Here a traditionally safe Tory seat is under attack from the energetic Lib Dem candidate, Mike Martin. These voters, to generalise, never rejected the Cameron brand of politics, as the West Midlands voters had. To them the problem with Ms Braverman wasn’t really her politics, it was the fact that she wasn’t a team player, and showed no particular signs of administrative competency. To people who are professionals themselves, as so many of these voters are, this is a cardinal sin. It is a point that the Brexit-supporting populists simply cannot understand. The professionals have warmed to Mr Sunak, who is well to the right of their normal politics, because he displays this professionalism – unlike his two immediate predecessors – Liz Truss and Boris Johnson. They abhorred former Labour leader Jeremy Corbyn with a passion, as he was the diametrical opposite of professional.

But, alas for Mr Sunak, Sir Keir is a consummate professional too. As is Sir Ed Davey, the Lib Dem leader – and indeed this group of voters rather liked the Lib Dem – Conservative coalition that Lord Cameron led, and probably like the idea of a Lib Dem-Labour one (anathema as that is to Sir Keir). Mr Sunak may have stopped a rout, but he will need to do more to secure a win.

To do that Mr Sunak will need to show that he is getting to grips with the crisis in public services, and the chaotic illegal immigration in small boats across the Channel. Pretty much all public services are in a sorry state, but the most important politically for now are the NHS, the courts and water and sewage (where problems are close to home in Tunbridge Wells). But to seize the initiative here Mr Sunak will need to unlock public spending, to invest in facilities and to restore lagging pay – otherwise he will not be seen as serious. This matters more than the tax cuts beloved of the Tory right. There is talk of cutting Inheritance Tax, as this is a wedge issue with Labour. Inheritance Tax does weigh heavily in the minds of the wealthier people of Tunbridge Wells, with its high property prices – but my guess is these voters would be unimpressed with such shameless politicking. The forthcoming Autumn Statement from the Chancellor of the Exchequer will be a critical test for this government.

But as Stephen Bush says, just as Mr Sunak was unable to capitalise on gestures to the populists because of his lack of follow-through, he will not capitalise on his gesture to voters of Tunbridge Wells for the same reason.

Last weekend The Observer reported that a senior Conservative had suggested that the Tories were in danger of being the “nasty party” again. They needed to show more humanity, he said. This followed some provocative language on the subject of asylum seekers from the Home Secretary and the party’s deputy chairman. The nasty party epithet resonates because it was attributed to the party during the long period of its doldrums while Tony Blair was prime minister, and and the party suffered three crushing defeats to Labour in general elections. It took a conscious rebranding effort by David Cameron to break free of the tainted Tory brand.

The Tory brand is undoubtedly deeply tainted once more. Their poll ratings are dire. Even in traditional heartlands, like where I live in rural Sussex, the party is being rejected in local elections by spectacular margins. Nice middle class people treat the party with disdain. The party’s main electoral strategy, though, is not to woo these voters but lower middle class and older working class voters who were part of the anti-establishment coalition that supported Brexit, and flocked to the party in 2019 in the “Get Brexit Done” election. It now seems that appealing to these voters is one of the driving principles of government policy, casting aside all considerations of national or wider interest. These voters are thought to like the “nasty party” image.

The problem of small boat crossings across the Channel illustrates the government predicament well. It is this flow of illegal immigrants that provoked those nasty comments. The government promotes a series of “tough” but token policies – such as trying to transport migrants to Rwanda, and housing them on a barge that looks distinctly like a prison ship. Ministers then attack “leftie lawyers” for slowing down (or even stymieing) these ideas, in the hope that mud will stick to Labour, led by lawyer Sir Keir Starmer. Certainly the flow of migrants across the Channel irritates Brexit-supporting voters, who are no sticklers for the rule of law.

But the flow of boats goes on. There is apparently a slight dip in numbers in 2023 compared to 2022, but this may just reflect weather conditions. The people traffickers are getting better organised, and are easily able to outwit government efforts to impede them. For some rather puzzling reason government ministers have been claiming that their policies are designed to “break the business model” of the traffickers. Perhaps they think this form of words sounds clever. But their policies are not directed at this goal at all. The business model depends on the absence of legal routes of migration, or even alternative illegal means – this forces migrants into the traffickers’ arms, allowing them to extract high prices and therefore invest significant money and effort in beating the government efforts efforts to make their lives difficult. Of course the government does not feel it can offer alternative routes, because that means letting more in legally, and their whole aim is to reduce flows overall.

And the longer the flows persist, the more the government has to confront difficult questions. The first of these is why all this is blowing up now, after Brexit, when Brexit was meant to enable Britain to “control its borders”. The business of managing borders is clearly a lot harder than most Brexit advocates had said. Then there is the the rather pathetic scale of the Rwanda and barge policies compared to the volume of incoming people: hundreds compared to tens of thousands. Worst of all is the effect of painfully slow processing of asylum claims, which has left tens of thousands in limbo, many having to be put up at state expense. What the government has not quite admitted was that this backlog arises from deliberate incompetence, as the former Home Secretary Priti Patel seems to have though that processing claims more slowly would reduce the incentives for people to come over and make claims. That hasn’t worked: instead state agencies and their political masters are made to look chronically ineffective.

Polls now show that few people think that the government will fail to stem the flow of boats. In the short term it might work for the Conservatives to deflect the anger towards the liberal “elites”, personified by leftie lawyers. But we probably have more than a year to wait before the next election. It is hardly worth suggesting that the opposition would do no better, when it doesn’t look as if things could get much worse.

If it is to turn the tide of opinion, the Conservatives needs to demonstrate competence above all else. Those nice middle class voters will forgive a lot of nastiness for that. Angry Brexiteers are not so dissimilar. And as for international standing, foreigners have their nasty side too – it is competence that inspires their respect. The problem for the party is that it has turned incompetence into something of a feature since they chose Boris Johnson as their leader. Both he and his successor, Liz Truss, openly selected cabinet ministers on the basis of loyalty rather than ability. Political posturing mattered above all.

Since then there have been an endless succession of ministers evidently not up to the job. Mr Sunak seemed to break from that idea. His stock (and the government’s) was never higher than when he reached a deal with the European Union over Northern Ireland – allowing competence to trump political posturing. But then again, his appointment of the inexperienced but ideological Suella Braverman as Home Secretary always pointed in a different way. Now political messaging is once again the priority, as the government stumbles from one mishap to another.

This recalls the government of John Major in the 1990s, with the party exhausted and fractious after the Thatcher years. It is true that this government managed to pull off an election win against the odds in 1992 – but at that point the government was being given the benefit of the doubt on its economic strategy, while doubts over Labour leader Neil Kinnock persisted. By 1997 the government’s haplessness was exposed to all, while his Labour opponent, Tony Blair, was the very picture of slick competence. Sir Keir can’t aspire to Mr Blair’s heights, but he looks competent enough. Mr Sunak’s supporters may keep clutching at straws (as did Mr Major’s “the darkest hour is just before the dawn”, they said, inaccurately) but it is heading for humiliation all the same.

After Jeremy Corbyn, Boris Johnson and Liz Truss, and the post-2017 version of Theresa May, most Britons have been yearning for a time when their main party leaders were ordinary competent politicians. But now Sir Keir Starmer has taken over the Labour Party and Rishi Sunak the Tories, that day has come. Both men had less political experience than their leadership positions normally warrant, and accordingly had uncertain starts, but now both are now hitting their stride. It promises to be a fascinating, if unedifying, contest, at least for those who follow politics as a spectator sport without worrying too much for the consequences for the country.

Sir Keir matured first. Indeed earlier this year he decided that he had to hammer Mr Sunak’s apparent weakness as hard as he could. I was uncomfortable with this: it didn’t matter to Sir Keir whether the attacks were well grounded or not – he ruthlessly went for the man rather than the policy. It seems unpatriotic to keep undermining your country’s prime minister just for the hell of it. But that’s politics – Mr Sunak would not hesitate to do the same if the roles were reversed.

Mr Sunak has survived this, and it is Sir Kier who has lost momentum as a result. The turning point came with his renegotiation of the Northern Ireland Protocol that had been spoiling relations with the European Union. This was a thoroughly competent piece of statecraft that moved things along. Few doubted that this deal was the best that Britain could get – and opponents seemed to be the sort that did not really want resolution at all. Better still, Mr Sunak was successful in selling this to his own party. Only 22 MPs voted against it in parliament – with many formerly troublesome Eurosceptics lining up behind Mr Sunak. That both Mr Johnson and Ms Truss were amongst those 22 underlined just how little threat his predecessors now pose. The deal has not convinced the Democratic Unionist Party to rejoin the Stormont government – but most observers thought that nothing was going to pass that test that would not cause even bigger problems in the province. In UK terms the DUP is very isolated.

That’s a good start. Mr Sunak had earlier set out five priority areas for his administration: inflation, NHS waiting lists, growth, national debt and “small boats” – the influx of illegal migrants across the Channel. It was widely assumed that his specific pledges on these issues were designed to be easy to pass – but with the economy poised on an awkward knife-edge, this should not be assumed. He needs to do two things if he is to a reasonable chance of winning the next general election, widely assumed to be in the autumn of 2024. The first is to win back the Brexit-voting, conservative working class and lower middle class voters that flocked to the party in 2019 – many of these are telling pollsters that they will abstain or vote for a protest party such as Reform UK. To these he needs to show that he is true to the Brexit vision, and especially on immigration; these voters, who tend to be older and retired, may be not so sensitive to the economy, but they are sensitive to the NHS and crime. The second thing is to win back or win over Labour- and Liberal Democrats-inclined floating voters with a less conservative political outlook, who generally voted Remain, but who were put off by Labour under Mr Corbyn. For these voters a display of competence is critical.

Sir Keir Starmer starts ahead, with substantial poll leads, following the Johnson and Truss fiascos. He may also have had a stroke of luck in Scotland. Scottish seats used to be critical to Labour’s success, but the party was wiped out there by the SNP in 2015, and then they struggled against resurgent Conservatives. But now the SNP seems to be imploding after Nicola Sturgeon’s resignation as leader. To watchers from south of the border this episode has all the hallmarks of a bloodletting and collapse after a long period of imposed stability – all Britain’s main parties experience this from time to time. Things are always a bit different in Scotland. Pro-independence voters don’t have many convincing alternatives – Alba and the Greens each have issues of their own. But the case for independence will have taken a temporary knock, and Labour is prevailing over the Conservatives in the anti-independence camp, with a stronger appeal to independence-waverers. A resurgence by Labour there would be doubly good news for Sir Keir. It makes winning an overall majority in the UK much easier for him, and it reduces the risk of the SNP holding the balance of power in a hung parliament – which would be a nightmare outcome, and a prospect that might scare the voters too. But for all this lead, Sir Keir knows that a lot can go wrong, and that the electoral system is in many ways tilted against him.

A lot of how the battle will play out is obvious. Labour will attack the government for incompetence on just about any issue that comes up, regardless of how justified the complaint may be. The Conservatives try to divert the blame onto world events and cast doubts on Labour as being soft lefties. Most of this be just noise to voters and unlikely to change minds. Beyond this I think there are two issues where voters’ are more open, and which could cause a shift in balance between the parties: tax and immigration.

Tax-and-spend arguments are as close as we’ll get to a debate over economic strategy. We will not get any kind of sensible discussion of economics, of course – even though there is an interesting debate to be had between the parties. Labour’s approach tends to focus on macro-economic policy. The priorities for them are ensuring that aggregate demand is sufficient to ensure low unemployment and decent bargaining conditions for workers, and getting decent headline figures for investment. The Tories rather focus on microeconomics – the idea that prosperity must be based on the efficiency of businesses and public agencies and how hard we work – where the question of incentives and competition loom large. Instead of that, the Conservatives will accuse Labour of wanting to dramatically increase public spending, leading to higher taxes and a less productive economy. They remember fondly John Major’s success with the “Tax Bombshell” campaign in the last week or so of the 1992 general election, when fortunes suddenly turned in their favour. The problem for Labour is that almost all public services are crying out for more spending, and it is very hard not to criticise the government without suggesting a substantial increase. Which leads to the question how you pay for it. This question is dealt with as if a nation’s budget operated like a household one, which is far from how it actually works. But it is too hard to try to explain that extra public spending might simply lead to better use of the economy’s resources and higher wages, and not necessarily to higher taxes. This argument is in any case a lot shakier when inflation is taking hold, as it is now.

The obvious answer is for Labour to try and sell the idea of higher taxes in order to have more effective public services at a time when the ratio of working people is falling. The tax burden may be at a historical high as a proportion of national income, but it is still moderate by European standards. There is even polling evidence that this has majority support. But Labour still carry the scars from 1992 (and indeed 2019) when the Conservatives successfully scared many floating voters with the prospect of higher taxes. Instead they want to follow Tony Blair’s and Gordon Brown’s strategy of 1997 of promising to hold back taxes and spending – and then increase both after the second term, when people are more used to the idea of a Labour government. Meanwhile they will try to dream up a number of painless taxes on other people to pay for selected areas of higher spending – non-doms, oil companies and so on. Against this the Conservatives will try to promise that better public services can come without higher taxes; since many voters are under financial stress, they will not relish the prospect of higher taxs. The arguments of both parties are unconvincing, and it is hard to see which way the public mood will swing.

Neither party is convincing on immigration either. There is panic over the number of people trying to cross the Channel in small boats, and then claiming asylum. Actually this is a real enough problem: overall numbers may be modest by the standards of international refugee flows, but it is placing public resources under pressure, and and it is a bit of a slam-dunk for organised crime. Immigration is not a top issue for voters according to opinion polls in the way it has been in the past. But both parties know that with the chaotic situation in the Channel, it can be pushed up the agenda easily enough. Housing the refugees (and others) while their claims are processed is creating stresses right across the country. Mr Sunak knows that he needs to do two things. To motivate conservative working class voters (and a lot of conservative middle class ones come to that), he needs to promote a tough line that will be hard for Labour to follow. The second thing is that he needs to make a substantial dent in the numbers making the crossing – to demonstrate competence, and woo back more liberal floating voters, as well as convincing those conservative voter that he isn’t just grandstanding. The first of these things is going well enough. The Home Secretary makes a good hate figure for liberal types, who make all the noise that Mr Sunak needs to demonstrate his toughness. But few understand how he is going to achieve much in the way of actual results, though. The much vaunted scheme to deport migrants to Rwanda does not look remotely adequate to deal with the sort of flows that we are seeing, even after the government has bulldozed the legal objections.

The Tories can sense Labour weakness here. Sir Keir has one sensible idea – to make legal routes for refugees more accessible, and the processing quicker, and so reduce demand and the numbers having to be put up in temporary accommodation. This means increasing legal flows of refugees, which will annoy many – but it does tackle the disorderly aspect of the current situation, which is what is most dangerous. But it is a stretch to think that this will stop the flow of channel boats by itself. The incentives for people traffickers remain strong. The only thing that might work there is rapid return of the migrants to France or elsewhere in Europe. But why would the Europeans agree to that? Only a substantial change to legal routes for refugees might possibly unlock that. that would be too brave.

It is hard to discern public attitudes to immigration post Brexit. There are two competing visions. The first is the Japanese one: that any immigration disturbs the cultural identity of the country and undermines social cohesion – as well as placing stress on housing and public services. So numbers of immigrants should be kept low, and definitely reduced. Or there is the Canadian/Australian vision, which accepts the desirability of substantial flows of immigrants, including refugees (at least in the case of the Canadians) – but wants the flow to be orderly – and abhors the idea of queue-jumping by unregulated arrivals. The small boats are abhorrent to both – but there any agreement ends. Both visions seem to have substantial support, and it is hard to see which way the zeitgeist will go. Labour seem to be more clearly pitching for the Australian/Canadian position, which is popular amongst the immigrant communities themselves – while the Conservatives are trying to play both visions at once. And as with tax, it is hard to see which side will end up on top.

There is a third issue which has the potential to sway voters: the environment. This covers not just the mission to reduce carbon emissions, but also threats to the countryside through habitat loss and pollution (and especially sewage overflows). The government is under attack for competence, as well as its heart not really being in it. But Mr Sunak has left it out of his five key targets – so presumably his party’s polling shows that this is not a critical issue. Labour are making a lot of the idea of green growth – but this may be more to motivate their core supporters than to win points over the opposition.

It will be an interesting contest. My guess is that sir Keir will prevail decisively. Whenever I try to write “Sunak” my computer changes it to “sunk”; I think he is, such is the low regard his party is held in by the voters..

Labour shortages mean that the pay of refuse workers is advancing

It turns out that the leaders of Britain’s Conservative and Labour parties agree on quite a lot. The latter, Sir Keir Starmer, gave a quite a weighty speech to the Confederation of British Industry this week – which did much to help his gravitas as prime-minister-in-waiting. What has drawn most attention is his opposition to excessive immigration (not clearly defined, of course) and commitment to making Britain a high-wage, high-productivity economy. This was one of the main planks of Tory policy in at least the last two general elections, and still is – in contrast to integration with the European Union’s labour and product markets. Many in the CBI want a more flexible approach to immigration (to say nothing of more integration with the EU) – but they weren’t getting it from either leader.

The politics are obvious. Immigration is a touchstone issue in Britain, as it is in much of the world. The public thinks that the ruling elite were too relaxed about immigration and this was one of the main factors behind the populist backlash of the last decade, and the Brexit referendum result in particular. Labour are less trusted by the public on the issue, and so need to show a visibly firm line, or they won’t win back the voters that have deserted them since their last election victory in 2005. And the idea that choking off cheap labour from abroad will raise living standards is superficially plausible. In fact it was one of the more plausible claims made by the supporters of Brexit. And having done Brexit, I can understand how mainstream politicians feel the need to try and make the idea work.

But how does political necessity fare against reality? Most people seem to have very little idea of how the high-wage economy is actually supposed to work. It’s a bit like the “Australian-style points system” to manage immigration, which most people think is a jolly good idea, without having much clue about what it actually is, and how it compares to alternatives. The main target audience for economic policy ideas seems to be property-owning retired folk in the English North and Midlands (and in the English South and Wales, to be fair), who have little direct stake in a modern, functioning economy – which is all somebody else’s problem. Meanwhile they insist that there is “no room” for more immigrants – and fear that it erodes English national culture. There is therefore no particular need to explain the actual impacts of policy.

The overall economic theory is clear. If we can raise economic productivity, there is more money per head to go round to support higher wages. By choking off the supply of cheap labour from abroad, employers will be forced to use the available resources, i.e. local workers, more productively. There are two basic problems with this line of argument. The first is that higher income per head on average does not guarantee higher income for everybody. An imbalance of power in the labour market leads to high pay for the powerful at the expense of the powerless. The hope is that cutting immigration strengthens the bargaining power of less powerful. Academics argue about whether it is true – but it is not hard to find anecdotal evidence of just this. A shortage of lorry drivers following Brexit has recently driven up their pay – and with it incomes workers in related fields, like refuse collection. Still, we shouldn’t forget, as Tories sometimes do, that better wages depend on the bargaining power of workers.The second problem is that productivity is only part of the equation – the proportion of working people, or working hours per head of the total population, is critical too. In fact in a modern developed economy it is probably more important – and it has been falling due to demographic pressures, the propensity of older workers to retire on their savings, and (perhaps) lack of access to health care for longer term and mental conditions. Immigration raises the ratio of working people in the short and medium term – which is why so many people think it is a good idea.

Still, let’s put these problems aside, and try to imagine what a high-wage society looks like. It is in fact not too hard to find such societies. They are usually located in spots in the developed world with a low population density. These are often tourist hotspots and it is mainly as a tourist that I have visited them: in Australia, New Zealand, Western Canada, Norway and Switzerland. The first thing you notice is that there aren’t many workers. If you are on safari in Africa, you will get a tour guide and driver as a minimum. In Canada and Australia the same individual does both roles. Go into a shop and there are few people to serve you. And there aren’t many shops. At hotels you carry your own bags. You get something of the Tesco automated checkout phenomenon. Self-service amounts to higher productivity for Tesco, but all they are doing is making you do more work for yourself. An experienced cashier is much quicker. In a high-wage economy you may find yourself eating at home instead of at restaurants – or inviting friends for drinks at home rather than trying to find a bar. The cost of services involving human contact is relatively higher.

So where are the workers? Not so many in the tourist spots, though there will be people delivering high-end products or services at quite a cost. They are mostly somewhere else, delivering highly productive goods or services. In Australia and Canada there is mining; in Norway there is oil; in Switzerland there is sophisticated manufacturing (chemicals and such) and banking. These are linked to exports, so that high-wage countries tend to be high-exporting ones, usually running trade surpluses.

Here’s the key. Some gains to wages for the less well off can be made by reducing profits and cutting top-level pay. But not enough and not sustainably. A large proportion of workers need to be employed in highly productive fields. If businesses simply raised prices to pay for higher wages, we end up where we started by putting so many things out of the reach of less well-off workers. But high productivity industries in the modern era are very productive indeed. They don’t employ many workers and usually need exports to to be sustainable.

And so we can start to see the characteristics of a high-wage economy. Workers must have strong market bargaining power, generally by being in short supply. There must be a strong, highly productive core to the economy, generating a substantial export trade (overall trade doesn’t need to be in surplus in theory – though in practice this often seems to be the case). And most people will have to put up with doing more things for themselves, as the price of services is high – and especially in rural areas. Taxes are also likely to be quite high to to support public services such as health and education – as a strong state underpinning of these, and an effective social safety net, is all part of the ethos – and supports the strong bargaining position of workers generally.

In Britain the problem is obvious. Labour shortages are improving the bargaining position of workers. We are moving towards a self-service economy as these labour shortages sweep through the hospitality industry amongst others. But what of the highly productive core? Here we are faced with a fleet of ships that have sailed. Fossil fuels are depleted and anyway a problem in the zero-carbon future. The country’s manufacturing has been hollowed out – the trade deficit is of very long standing. Financial services provided a lot of punch in the earlier years of the 21st century, but are going through rough patch in the 2020s. Brexit is widely blamed, but in truth the problems are wider. A lot of the strength of the mid-noughties turned out to be fictional – and it was very centred on London. The country needs to look to the future, and not try to recreate old glories. Here the parties do differ a bit. There doesn’t seem to be a coherent Conservative strategy at all. Their basic idea is to create fruitful conditions for investment and sit back and wait. Liz Truss, Mr Sunak’s predecessor, did lend some coherence to this approach. She wanted to create a low-tax, low-regulation haven for footloose international businesses. This idea quickly collapsed, leaving Mr Sunak plying platitudes about innovation. His government looks increasingly paralysed by internal divisions and unable to implement any decisive strategy.

Labour’s big idea is the green economy (something promoted by the Lib Dems and Greens too). This entails a massive investment programme designed to transform the country’s infrastructure as well as develop export industries. This is a good idea, but a lot of the work involved (home insulation for example) is not high-productivity. And there is intense competition for the rest – batteries and wind turbines for example. Still, it doesn’t do to underestimate British inventiveness, and public-private partnerships in this area surely provide part of the answer. Also renewable energy does offer high productivity, without the need for exports. There are other ideas. I have often talked about health care and related services, where Britain has a promising base – and where the NHS offers world-class data for developing new treatments – as the covid episode showed.

But there is a gorilla in the room that the politicians don’t want to talk about. This isn’t Brexit (though they don’t want to talk about that either). This has created problems for developing export industries – but other EU members are further down the path of developing exports and British industries struggled to compete with them in the single market. Britain’s trading problems got worse within the EU, after all, even if there were compensations. The gorilla is public sector pay – especially if we include the issue of social care. High wages mean high levels of pay in the public sector. Not all public sector jobs are badly paid, but the pressure of a tight labour market is putting public services sector under pressure. Staffing shortages are rife in many parts of it. Meanwhile part of the government’s anti-inflation strategy is to hold back public sector real pay levels – which is making matters worse. The answer is either to shrink the public sector or to raise taxes. Of course the politicians hope that an explosion of high-productivity private sector jobs (with associated tax revenue) will come to their rescue. But it won’t happen in time, if it ever does.

This is a tough place to be in, so it’s no surprise that our politicians are slow to confront the truth of it. I have to admit that it is forcing me to rethink some of my assumptions. But I do think that the vision of a high-wage economy is worth pursuing. The main alternative being offered by those interested in social equity is a universal basic income paid by the state. I am deeply uncomfortable with that idea for a number of reasons. Given that, here are two things to be thinking about.

The first doesn’t involve any great rethinking on my part, but remains politically toxic. We need higher taxes. This is not just on various soft-spots and loop-holes in the wealthier parts of the economy – schemes that are predestined to disappoint. Higher taxes need to affect most people. This is because public spending will have to rise to accommodate higher public sector pay – and we need to manage down the level of demand in the rest of the economy to help stabilise it, to say nothing of limiting the need to borrow money on world markets. Of course public sector productivity can be improved (though I prefer the word “effectiveness” to “productivity” – as a lot of the solution is lowering demand by forestalling problems), reducing the need for spending. But our political class, our civil servants, and the commentators and think tankers that critique them, have almost no idea how to achieve this. They are stuck in an over-centralised, departmental mindset. What is needed is locally led, locally accountable, cross-functional, and client-centred services – an idea that is so alien to British political culture that most people can’t even imagine it. So we can’t count on that idea and must settle for replacing the dysfunctional with the merely mediocre, with no cost-saving.

The second idea is even more contentious, and I haven’t properly thought it through yet. It is that inflation is an essential part of the process of readjustment, and we have to tolerate it to a degree – provided that the source of that inflation is a rise in pay for the less well-off. As somebody who grew up in the 1970s, I hate inflation. I think it undermines trust between the state and the governed. I have never subscribed to the view of liberal economists that it can be a tool of economic management. But there have to be exceptions. One example was Ireland in the 2000s, as that country worked through its economic transformation as it integrated with the EU economy, which did involve a spurt in productivity. Wages rocketed, driving inflation up. Ireland was in the Euro, so there was no ability for the currency to appreciate to ameliorate the effect. This was the only way for the country to reach the sunlit uplands – which didn’t stop the European Central Bank from criticising it – something my economics lecturer at UCL said was absurd.

Britain’s position is different from Ireland’s. We haven’t had that productivity spurt. There is nothing to drive an appreciation of the currency. But we want wages amongst the less well-off to rise. Price rises are part of the adjustment – with inflation acting as a tax on the wealthy, as part of a redistribution process. Meanwhile we need to drive capital investment – most renewable energy is very capital intensive, for example – as are most of the ideas for developing higher productivity. That means keeping interest rates low. Which won’t happen if interest rates are jacked up to combat inflation. And, as suggested already, to the extent that inflation needs to be managed, higher taxes are a better way to do it.

This is quite a progression in my personal thinking (and thank you to regular commenter Peter Martin for helping me along the way – though doubtless we still disagree). But trying to get to the fairer, more sustainable society we seek is going to require many of us to change our thinking – and put up with some things we don’t like.

When Theresa May went to the country in the general election of 2017, she promoted herself under the slogan of “strong and stable”. Polls showed the Conservatives heading for a massive landslide. Polling day came a few weeks later, and the party lost its majority. British politics has not settled down since. The “strong and stable” label for the Tories has never looked less appropriate, though that won’t stop the party from trying to use a version of it again. Reliable predictions are impossible, but it’s still worth trying to get some idea about how things could develop from here.

When Boris Johnson won his landslide for the Conservatives in December 2019, it was commonplace to suggest that it would be impossible for Labour to come back to winning a majority in one go. I always thought that was nonsense – an example of the human cognitive bias towards the status quo. It was suggested that a turnaround on such a scale would be unprecedented. So what? Less than three years later under Liz Truss, Conservative polling plumbed to such depths as to suggest not only a Labour majority, but a landslide. Now she’s gone, and the dust has far from settled.

Slowly the poll ratings are coming back to the Tories, but the Labour lead remains massive. The new Conservative leader, Rishi Sunak, is regarded much more favourably than his predecessor by the public, especially on the critical area of economic competence. It is possible to sketch out a scenario whereby he manages to claw his party back to winning a majority at the next election. Economic competence is at the centre of such a scenario.

Now it is important to understand how the public perceives economic competence. It has little to do with actual competence. The critical signs for the public are keeping a tight reign on public spending, and also for the economy not to be subject to dramatic adverse changes. Economic growth does not count for as much as many people seem to think. The bedrock of Tory support is retired. They have paid off their mortgages, have substantial value in their houses, and receive reasonably secure pension income, some of it from the state. They don’t like higher taxes because their income is relatively fixed. But unemployment, higher interest rates, and so on hurt them little. They shrugged at warnings that Brexit would damage the economy, and still do, even as many of the warnings are being realised. They are for economic growth in theory, but against just about any policy that will bring it about. There aren’t enough such people to produce a winning majority, but without them, or a substantial majority of them, the Tories cannot win. Labour under Tony Blair wooed enough of them over to put the Conservatives out of power for more than a decade.

On top of this bedrock the Tories need to win over another swathe of voters with conservative instincts. These are more aspirational; they have jobs (usually in the private sector) and own their homes, or feel that home ownership is within reach. This group is going to be put under pressure by higher interest rates. Mr Sunak may escape blame for the current rise in rates, justifiably or not, thanks to the political ineptitude of his predecessor. But it’s important that the rates don’t keep going up. That means running a conservative fiscal policy. Both he, and his Chancellor of the Exchequer, Jeremy Hunt, seem to understand this. If inflation turns a corner, thanks to easing world conditions for energy and food, the pressure on interest rates will ease and it will look as if the government has managed a crisis well. The Tories would be in a position to raise doubts about Labour or a “coalition of chaos”, and, combined with the redrawing of parliamentary boundaries, there lies a narrow path back.

The threat to Labour of such a scenario is real enough. The public retains a serious bias against the party on economic management. This was made worse during Jeremy Corbyn’s tenure as leader. This wasn’t so much from what he and the party actually said – his shadow chancellor, John McDonnell, proved to be an able communicator – than from a general attitude by the party that used the word “austerity” as a term of abuse. The party made no attempt to pick fights with interest groups on the grounds that “we can’t afford that”. Things are much better under Sir Keir Starmer, though he has not picked able communicators as shadow chancellors – the best that can be said of the current incumbent, Rachel Reeves, is that she is more effective than her predecessor, Anneliese Dodds. Their strategy seems to be, as it was under Mr Blair and Gordon Brown, “the same, only different”: trying to pick only carefully chosen and relatively minor differences, like windfall taxes, but copying Tory policy otherwise. When Tory policy goes crazy, as it did under Ms Truss, this leaves them looking muddled. They were much happier under Boris Johnson, who tried to dodge hard choices altogether, meaning theatre was less pressure on Labour to confront choices it would rather not. Labour will face an awkward strategic challenge under the Sunak-Hunt regime. The “same, only different” strategy is still viable, but it will pose some awkward choices on its attitudes to public spending.

Mr Sunak is left with two major headaches, though. The first is on public services. The government will be forced to constrain resources in order to manage the budget deficit. The timing is awful. Services across the board – health, education, the police, courts, to name only the most obvious – are all under stress, and they are about to be put under further pressure by workers demanding that pay keeps pace with inflation. The job market remains quite tight, so retaining staff is going to be hard. And these public services, mostly, matter to people. The obvious cuts have already been made, and saving money through more competent management is something this government seems to be unable to pull off – years of incompetent leadership are a large part of how they got into this mess. Politicians have lived too long on the notion that message and narrative matter more than operational effectiveness. The government could face constant distraction from one public service crisis to the next, giving the overall impression that they have been in power too long and their time is up. They won’t be able to rely on trying to divert the focus to Labour.

The second problem for Mr Sunak is related: his party lacks competence and discipline. Crisis in public services could be compounded by parliamentary rebellions and questions over his leadership. His need to maintain a broad church of views within the cabinet does not help. Trouble with the Home Secretary, Suella Braverman, illustrates this. She goes down a storm with party activists, and helps keep the culture wars burning – but tub-thumping will help little in trying to run a complex and important brief, which has already suffered from years of poor leadership. She had already been sacked by Ms Truss for what amounted to gross disloyalty (thinly disguised as breach of ministerial procedure). She is more a politician than an administrator. But on the backbenches she could be a thorn in her leader’s side.

To people like me, it is hard not to think that these are symptoms of a political system that may have worked once, but which has long since ceased to do so. Politicians achieve high office by playing the gallery to a small coterie of deranged activists and donors, and where administrative competence and negotiating skills count for little. So it is disappointing that Labour are offering no serious political reform. Activists support the introduction of proportional representation, but Sir Kir has no intention of letting that get into his manifesto. He is worried that marginal conservative voters will react against it. That may be a sound judgement. Perhaps if a coalition is forced on him by the Liberal Democrats, he will entertain some degree of reform. There may be something in Tony Blair’s strategy of being cautious before winning power for the first time, and more radical on the next occasion. But for now it is hard to know whether the Labour party is on the right strategic course, and has enough competent people at the top. To me it looks vulnerable.

But there are good odds on Sir Keir being the next prime minister – and that looks justified.

This week’s Bagehot column in The Economist suggests that Labour’s policy of freezing energy prices is bad policy (actually “silly”) but good politics. It says that Labour has been too tied to “wonkery” – the design of policies that are clever enough to solve problems without the need to confront awkward choices. Their new policy is a welcome break form the current Labour leader, Sir Keir Starmer. But I don’t think the policy is quite so silly – even if Labour’s suggestions about how the costs will be managed mainly are.

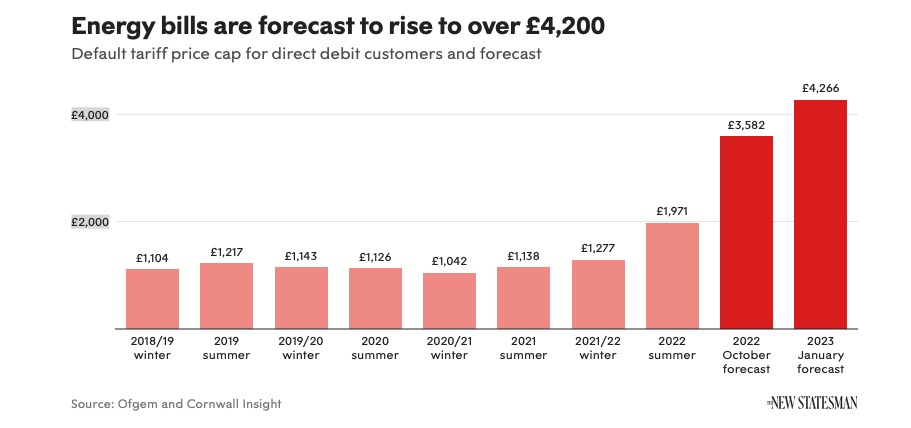

The challenge is huge. British energy prices, especially for gas, have shot up this year. But that is just a foretaste. Further steep rises are in the pipeline: the graphic above, showing annualised costs, culled from the New Statesman (featuring widely quoted projections from Cornwall Insight – who seem to be the only people making them) shows the problem. The median annual household income is estimated to be £31,400 after tax – so costs are rising from 4% to maybe nearly 14% of income for the median household, and it could be double this for the bottom quartile. Other costs are rising too, and, for most people, pay is not keeping up (many senior executives and our local refuse collectors excluded). The media has little difficulty in finding cases of extreme hardship – of people choosing between energy and food for example – and, apparently, not even being able to heat that food up. In one case publicised by BBC News, somebody was selling their furniture to pay their bills. And that is before the forecast price rises have gone through, and before winter brings in the need for heating. Overwhelmingly the public feel that the government should step in to relieve hardship – although how many Conservative Party members share this feeling, while they choose their next leader, is not clear. So far, so clear.

This is where The Economist‘s wonkery comes in. The view amongst Britain’s policy wonks is that help needs to be concentrated on those that need it most. Trying to cap the price for everybody, a policy widely favoured in other European countries, is regarded as a bad idea. For two reasons: first it wastes public funds on people that don’t need it, and second it blunts the market signal that people should reduce energy consumption, and so ease the imbalance between supply and demand that is causing the problem in the first place. This thinking has guided government policy to date. British energy prices have been allowed to shoot ahead of those in the rest of Europe – while the government is trying to target the bulk of its help to the neediest. But this bumps into a major problem. How can the government tell who to help, and who can get along without it? They have two main ways of trying to do this. The first is to help those already entitled to other help, such as Universal Credit – and the second is to ask people to apply for help, and then to assess whether they actually need it.

Both solutions are badly flawed. A problem on this scale is going to hit many people not entitled to benefits, which have become notably stingier over time. I have seen this problem in a different context: the supply of free school meals to struggling families. Many families need the help but are just above the threshold for entitlement. The problem with asking people to come forward is that many will refuse to as a matter of pride, while others who don’t need the help will try their luck, and need to be weeded out in some way, or else the system will subject to allegations of widespread abuse. This last has been the case with help for businesses in the pandemic. This problem is what I have called the Information Gap. The state does not know enough about individuals or businesses to tailor its policies to specific need. It either creates universal entitlements, helping those who are not in need, or resorts to a number of very blunt instruments, which often create political backwash.

The Information Gap is not just some technical problem that can be left to policy wonks to solve. It is one of the central problems of the modern state, and everybody in politics, wonk or not, should be aware of it. There are three general philosophical approaches to dealing with the Gap. One is to use the best efforts of the state to gather information and close the gap, compelling disclosure as required. This is the approach we associate with the Chinese Communist Party; it is highly paternalistic, and seamlessly moves into the state intruding into our private lives in unexpected ways. And the state never gets enough information to solve the problem properly. Its opposite is the libertarian approach. This suggests that the state should not involve itself in helping individuals at all. It should establish a system of security and property rights, and not much else. This thinking is popular n the political right, though not amongst populists. The third approach is solve the problem through a combination of universal entitlements and high taxes. This has recently been popularised through the advocacy of Universal Basic Income. Of course nobody, or almost nobody, advocates taking any of these three approaches to the extreme. Practical statecraft involves balancing all three approaches. Politically, though, we need to develop a sense of in which direction is the site needs to tilt at the current time.

Alas politicians rarely succeed by being honest about the difficult choices involved. Tory leadership contender Rishi Sunak seems to be suggesting that we take the more paternalist approach – but without being clear as to how the information gap is to be closed. His past behaviour in the pandemic suggests that we will accept a high degree of failure and try to shrug it off. His rival, Liz Truss, is suggesting a more libertarian approach – but without being honest about the widespread hardship and business failure that is likely to result. And now Labour is suggesting the use of universal entitlements – but without being honest that this will lead to higher taxes. All three are displaying a dependence on magical thinking. Labour’s “costing” of its new policy is laughable – but the economic illiteracy it is showing is the rule amongst serious politicians, not an aberration.

Personally I think Britain needs to move further along the universal entitlements and high tax route – an approach derided by Ms Truss, but one which the better-run European states favour. That does lead to further problems. Public services will require more discipline to improve their effectiveness, which I believe will have to come alongside decentralisation – with political accountability moving in parallel. That will require deep reforms that people may support in theory, but will resist in practice. Without reform, services will simply gobble up resources without becoming more effective. A further problem, shown in other European countries, is that tensions over immigration have to be managed. If entitlements are high, the public resents people it sees as freeloaders – and there is political mileage in stoking up that resentment, whether fair or not.

So that’s two cheers for Labour – and indeed the Lib Dems whose policies Labour seem to be copying. Alas I don’t see any sign that either party is going to be honest about taxes. But the public, surely, will start to see the need for hard choices. The careers of the two British politicians most egregious in suggesting that no hard choices are required – Boris Johnson and Jeremy Corbyn – have both ended ignominiously.

Hardly for the first time in my life, I have got something wrong. In my recent post on the Conservative leadership contest I suggested that Rishi Sunak would prevail over Liz Truss. This was based on the thought that Conservative members were more sensible than they are usually portrayed to be, and that they would react against the apparent recklessness of Ms Truss – t and favour Mr Sunak’s better presentation skills. I have badly underestimated Ms Truss, as I now think she is unstoppable, but I’m hardly the first person to do so.

Monday night’s TV debate showed why. Mr Sunak badly needed to portray Ms Truss’s economic plans as reckless (an opinion which I share), and especially that they could send inflation and interest rates up. He got his point across pretty successfully. In the process we found him talking over his opponent repeatedly with the confident male assurance that far too many of us have seen senior men do with female colleagues. Would he have done that with a male opponent? You bet he would – he was desperate to convey his message. So it probably wasn’t sexism – it was the opposite, not making concessions to Ms Truss’s sex. But it was a very bad look, and looks matter. Ms Truss held her line firmly; the waves broke over a rock. She had ripostes prepared, and she used them. Mr Sunak’s plans were contractionary (er… that goes with taming inflation); it was all Project Fear (a clever reference to the Remain campaign’s warnings of the economic consequences of Brexit – which have largely been proved right, but which Mr Sunak could not point out); it was all Treasury conservatism and “bean-counting” (true enough – but not actually relevant in this context). She surely did enough to cast doubt in Conservative members’ minds about Mr Sunak’s plans. Meanwhile Mr Sunak’s behaviour neutralised his actually rather impressive confidence and command.

This is a race between the tortoise and the hare, that we have so often seen played out in politics. The patient plotter quietly and relentlessly pursuing their ambitions, while their flashier opponents fall apart one by one. John Major; Gordon Brown; Theresa May – (you can go back further – Jim Callaghan; Ted Heath; Clement Attlee). Like all of these, Ms Truss has endured massive amounts of sneering criticism on her journey upwards. Apart from Attlee, though, none of them were particularly successful once they achieved the summit of their ambitions.

I have in fact met Ms Truss. It was before she was an MP, when she was attending a Lib Dem conference in the later 2000s on behalf of Reform, a think thank devoted to new ideas for public services. We exchanged pleasantries, but I don’t remember much beyond that. Reform’s ideas were (and still are) definitely centre-right – and more to the right in those days of New Labour. They favoured the conversion of state schools to academies, for example – something of a red herring in policy terms. As I remember they had better ideas elsewhere – they had a god line of constructive criticism. This part of Ms Truss’s career tells us two things. First is that she is fluent in the world of think tanks and policy debate. She is repeatedly portrayed as being a bit dim: this is far from true – but it is harder to shake the accusation of shallowness. The second thing this tells is us is that she is a professional politician, and knows no other trade. She was in her late 20s at this stage – was elected to parliament in 2010 and quickly became a junior minister (in 2012), reaching the cabinet in 2014. To be fair, she did train as a management accountant (i.e. a qualified bean-counter, like me, though working in business rather than in the profession) – but she did not take up any serious professional or management role. Her whole life seems to have been political – with politically active parents, and active with the Liberal Democrats at university, before taking up with the Conservatives. She paints this as a political journey, rather than opportunism – and I’m happy to take her word on this. I’m told she was never a left-wing Lib Dem, and the Conservative Party is in the long run a happier place for economic liberals – though deeply out of fashion in the 1990s. But a political career was clearly always on her mind.

Where does this leave us? We have no reason to doubt her conviction to a particular political philosophy (unlike Boris Johnson, for example) – that of being an economic liberal. But her attachment to particular policies never seems to be very strong. She knows all about how to win power, but her ideas about how to exercise it have less “bottom”. This isn’t all bad – disaster can happen when a particular politician has an idée fixe, which they pursue obsessively regardless of evidence. A particular disaster was Andrew Lansley, the first Health Secretary in the coalition government of 2010, who implemented an over-engineered reform of the NHS when it was already suffering reform fatigue. Ms Truss might have the flexibility to change course when things go wrong. The danger is that her yardstick of success is less about actual achievement than the political mood. She is not a conviction politician like Margaret Thatcher. If she was, she would have been completely thrown by Brexit, which she energetically opposed, and now supports with equal energy.

Getting the top job, if she succeeds, is going to be a big shock for her. You can’t get away with sleight of hand. If the economy goes seriously wrong, for example, she can’t simple vanish and blame somebody else. She may be comfortable with rapid changes of course, but she would then find it harder to persuade people to trust her. She is a poor public speaker, verging on disastrous. This was one reason that many people, including me, never took her chances of rising to the top seriously. She simply did not look the part.

As my readers will know, I think her ideas for tax cuts will be disastrous. They will hinder the fight against inflation, which will lead to increasing interest rates. They are a gamble that you can fight inflation without damaging economic growth. Given the obstacles the country is experiencing international trade and labour markets, not least by Brexit, this looks unrealistic. She may well be forced into austerity policies, including public service cuts just as an election looms.

So if I was a Conservative member I would choose Mr Sunak. But Ms Truss has been running this race for much longer than him. And it shows.

I’ve been away on holiday for the last week, near Bakewell in the beautiful Peak District of Derbyshire. So I haven’t commented on the race to succeed Boris Johnson as leader of the Conservative Party – which under the UK’s unwritten constitution means the automatic assumption of the office of Prime Minister. I did watch (most of) the two televised debates. You will have to take my word for it that I was predicting that the final two would be Rishi Sunak and Liz Truss even as Penny Maudaunt was the 58% betting favourite to win the whole thing.

As I write, Ms Maudaunt may yet make it to the final two, to be decided by party members, and even Mr Sunak’s place there is not guaranteed. But let’s assume that things turn out as I predicted. Which one is likely to win overall? This is hard to predict. YouGov have made a valiant attempt as polling Conservative members, but to get their sample they are fishing in a large lake for a rare fish. Their polling suggests that Ms Truss has a comfortable lead. This fits with most commentators’ prejudices of the Tory membership, as most think they will prefer Ms Truss’s more ideological pitch – or may even be worried by Mr Sunak’s ethnicity. Actually I’m not so sure, and I expect Mr Sunak to prevail in the end.

These two candidates were always the strongest in the field of seven candidates left after Jeremy Hunt was eliminated. They have both held one of the great offices of state (indeed Ms Truss is still Foreign Secretary), and they are both well grounded in the sorts of choices governments have to make. The other candidates have come up with interesting debating points but show little evidence of actual grasp. Meanwhile both Mr Sunak and Ms Truss have come closest to putting forward coherent policy positions – and they clash. Mr Sunak has taken the continuity position, of keeping taxes and spending much as they are, and defending the various measures put forward to relieve hardship as the cost of living crisis takes hold. This makes sense as he was Chancellor of the Exchequer until very recently. This has been heavily criticised by Ms Truss. She says that the tax rises (National Insurance is going up, alongside Corporation Tax rates) will cause recession. Instead tax should be cut in the short term, to generate economic growth. Inflation should be curbed by the Bank of England – whom she suggested were in large part responsible for inflation in the first place.

Three questions are posed by this challenge. First, will tax cuts generate growth? Second, can Britain afford more public debt? And third, is the fight against inflation best left to the central bank? The first question is in fact quite complex one – and politicians of left and right often try to hide in the complexity to justify populist policies of lower taxes or higher spending.

There are a number of ways that tax cuts can stimulate growth. The most direct is by allowing people to spend more (assuming that it isn’t accompanied by public spending cuts) – which helps take up economic slack. Donald Trump’s tax cuts worked like this, at least to some extent. But there is very little sign of slack in the UK economy. Indeed this is one of the causes of the inflation crisis. Tax cuts will either fuel inflation or suck in imports (and the country is running a current account deficit). A second mechanism for tax to affect growth is by drawing in more capital – fixed or human – by improving incentives. The case for this is strongest for Corporation Tax – as this is something multinational companies factor into their choice of where in the world to invest – but there is little evidence that it is a big factor in the UK. But Corporation Tax is a very efficient tax, and low interest rates are keeping costs of investment generally low. There is in any case a big time lag between any tax cut and any change to investment behaviour – it will have little effect on whether the country avoids recession this year or next. The question of incentives for income taxes is much less clear – it is a classic essay question for first-year economics students. Lower taxes make work more rewarding increasing the incentive to do more, but also the could reduce the need to work to fund your chosen standard of living. If tax rates are very high (for example, the top rate of 83% current when I was calculating payroll deductions in 1976) the chances are that the former predominates – but the case is much harder to make at current levels. Tax cuts won’t help growth, especially in the short to medium term.

Can Britain afford to borrow more, meaning that it is easier to cut taxes without cutting spending too? The Conservatives promised not to do this in their 2019 manifesto. But Ms Truss suggests that we can get round this by classifying a chunk of debt as “Covid debt” to be paid off over a longer time frame. Mr Sunak says this is nonsense. Running a budget deficit in a country that controls its own currency isn’t necessarily a bad thing – it does not work like a household budget. If there is slack in the rest of the economy it is almost a national duty. And there is the argument that if the markets can’t stomach it, you can simply create the shortfall as money. But this can be inflationary, and there comes a point when the providers of finance insist on lending in other currencies. Britain has not been in anything like this danger zone since the early 1980s, when deficits from nationalised industries caused havoc to government finances. Inflation has made the picture more complicated, and debt levels are historically high (in part thanks to the covid crisis). But Ms Truss is probably right on this one – if you can deal with the arguments on inflation.

And here Ms Truss says the Bank of England can take more of the strain in turning the tide. Indeed she has suggested that the bank is partly to blame for the inflation crisis in the first place. In one of the debates she suggested that the Bank’s mandate should be modelled on that of the Bank of Japan. It is hard to credit this. The only way that the bank can fight inflation is to raise interest rates. This restrains growth – indeed the policy makes no distinction between restraining growth and restraining inflation – it tackles one through the other. From somebody who is suggesting that the problem is a lack of growth this is an extraordinary line to take. Further, the inflation problem has largely been brought about by problems on the supply side of the economy (oil/gas problems, Brexit, covid and a spate of early retirements in the workforce). It is hard to see how higher interest rates would have helped. It is simply a shallow attempt at blame shifting.

But none of the leadership contenders have wanted to confront the economic reality of Britain’s position. Britain’s workforce relative to its total population is shrinking due to demographic changes. Those same changes are placing public services under greater pressure, especially in health and social care. There are no soft spots on public spending – squeezing local authorities and benefits merely puts other services, especially the NHS and police, under yet more pressure. We have cut too much on defence. There is no productivity bonanza that will make public spending more affordable – or to be more precise, improvements in productivity are affecting a shrinking share of the economy, and cannot be expected to provide a get-out-of-jail-free card. All that points to higher taxes, or taking the country down the route of high inflation and currency and debt crises. By suggesting that he will only look at tax cuts once inflation has been dealt with, at least Mr Sunak has one foot on the ground. In the land of the blind, the one-eyed is king.

Funnily enough I have more sympathy with the Tory position than most on the left. Public spending (and taxes) should be subject to continual challenge. It is lazy to shrug our shoulders and suggest that nothing can be done. it is better for people to make their own choices n expenditure. There is a huge challenge in making public services more effective and accountable. But fantasy economics does not help.

Maybe it’s one of those aging things, like the policemen getting younger – but to me our country’s political leaders seem to be becoming more overtly political. I thought that of Tony Blair’s New Labour in 1997, who set the trend for leaders since. And now our current prime minister, Boris Johnson, has taken it to a previously unthinkable extreme. This is evident in yesterday’s statement by Rishi Sunak, the Chancellor. The politics was blatant; a clear strategy for making the country a better place was not.

Mr Sunak was once a rising star in British politics, but now he look as if he will join the long list of politicians (and others) whose careers have been indelibly tarnished by association with Mr Johnson. Yesterday’s effort did not measure up to the difficult economic situation that so many people in the country face – and he instead focused on a number of core interest groups that the conservatives hope will secure them another general election victory, through their votes or donations. This was all too transparent, and not helped by Mr Sunak’s ridiculous claims, such as that he was a tax-cutting Chancellor.

To be fair, the government’s job in managing the economy is unusually difficult right now. Managing a modern economy is like riding a bronco – it is mostly about responding to collective decisions made by individuals and businesses, inside and outside the country, that can quickly overwhelm the tax and spending measures that are the government’s main tools of control. The government’s difficulties are not really of its own making on this occasion. The root causes are the covid-19 pandemic, the war in Ukraine and the ongoing challenge of climate change. These have delivered a series of economic shocks of a type that policymakers are completely unused to dealing with. The pandemic delivered a major but temporary shock to demand – and the government won plaudits for its drastic policies, like the furlough scheme to underwrite jobs. But it also dealt a huge blow to world supply chains, and that is what policymakers were unready for. From the 1990s onwards new technologies and globalisation bequeathed a highly flexible system of global supply, which people have taken for granted. Even before the pandemic these changes were going into reverse. As demand recovered from the shock, supply did not recover as quickly – and inflation is the result. The problem emerged in 2021, but policymakers responded with denial – including the politically independent central bankers. Nobody seems to know what to do. The last time anything like this happened was in the 1970s, and that was a very different world.

The government is faced with three big and immediate problems: benefits, public sector pay and help for people on lower incomes. Costs for basics, such as food, fuel and heating are rising much faster than incomes and this is creating widespread hardship. The government’s response is to offer some help to working people on lower incomes (provided they are above the minimum tax threshold), and that is about it. Government services are not being given additional budgets to deal with additional pay demands; benefits are being uplifted by a wholly outdated figure for inflation. Most of the help being offered is in fact an offset to rises in National Insurance contributions (NICs) (by changing the rate of pay at which NICs kick in), rather than an actual cut – though at least this targets lower incomes better than deferring the rises altogether. A summer of hardship lies ahead. The country is facing a big squeeze on living standards, and poorer people will feel this the most.

There are two main constraints to the government using the public purse to alleviate hardship. The first is the balance of supply and demand. If the economy cannot deliver the goods and services paid for by government largesse, then inflation will result, with the potential for a wage-price spiral. That was not a problem in the early phase of the pandemic, when government support was very generous, as private demand plummeted even faster than capacity to supply. It is clearly a problem now, and tricky to offset with tax rises, as these tend to affect demand less if they target the better. The second constraint is on public finances – the government’s ability to raise funds if spending outstrips taxation. It is a lot less clear that this is in fact a problem, though levels of public debt are high, and the Bank of England cannot help out by buying bonds through Quantitive Easing, as it could until recently. Still, solutions have been suggested, such as a windfall tax on oil and gas producers operating in Britain’s North Sea. The case for such a tax is a very strong one, but it is completely contrary to Treasury orthodoxy. This holds that it undermines the climate for business investment. In fact investment in oil and gas production in the UK has been very low. The government may feel that it wants that to change, with businesses investing their windfall profits in increasing production to make up reduced supply from Russia. But the government is hardly waving a big stick in order to get such a response.

I can accept that these constraints, especially the inflation risk, are real. But the crisis on living standards demands the taking of bigger risks with the economy than the government is willing to contemplate. In particular bringing forward increases to benefits for inflation looked like a no-brainer. The government’s thinking on that seems to be guided by pure politics. People on benefits (apart from pensioners) don’t vote Conservative and aren’t likely to. Instead the government is focusing help on people in work, and especially those with some stake in property (it is temporarily reducing property taxes, announced before yesterday’s statement). Pensioners are being spared the increase in NICs (which they are exempt from), and doubtless their incomes will catch up later in the parliament, using the “triple-lock” system of increasing the state pension.

Most remarkable of the measures announced yesterday was Mr Sunak’s plan to cut the rate of income tax in two year’s time. Given the ever-growing pressure on public services, it is hard to see how this can possibly be justified, except as a short-term gimmick for electoral advantage. It leaves me feeling exasperated. I am retired and drawing a generous private-sector pension (I’m not old enough for the state one). I was never going to suffer the increase in NICs, but I’m still going to benefit from the Council tax rebate, the fuel duty rebate, and, if it comes, the reduced rate in income tax. I am not facing any kind of hardship. This just doesn’t seem fair.

Will Mr Johnson get away with it? Labour is better placed to capitalise on the unfairness than it was when led by Jeremy Corbyn, but it is still tricky for them. There a still a broad swathe of conservative voters out there ready to be persuaded that people on benefits have only themselves to blame. But I think that pressure on public services, which now includes demand to increase our armed forces, is going to be very hard for the government to manage. Eventually reality will strike.

But in the short-term I think it will be Mr Sunak who will pay the political price rather than his boss.

Contrary to some of the headlines, yesterday’s British Budget was an austerity budget. Its aim was to bring current spending and taxes into balance in three years, with a capital deficit restricted to 3% of GDP. With the current budget deficit at around 11% of GDP, that is a sharp contraction. The Institute of Fiscal Studies points out that most households will be worse off next year. The ratio of tax to GDP is widely projected to be the highest since the years of postwar austerity. Austerity is what current economic conditions demand. The main risk is that it will not be enough, and that it will precipitate a recession in the run up to the next general election.

That the Budget felt the opposite is down mainly to brazen but effective news management by the Chancellor of the Exchequer, Rishi Sunak, and also to a stroke of good fortune. The main bad news was the substantial rise in National Insurance, alongside the withdrawal of most of the emergency support for Covid, notably an uplift in Universal Credit and the furlough scheme. This news had been broken weeks ago, and presented as in the former case a bold stroke to deal with the growing crisis in social care, and in the latter as the coming to an end of the pandemic nightmare. The stroke of good luck was that the independent Office for Budget Responsibility that produces the economic forecasts on which the Budget is base offered a more optimistic picture of the years ahead than hitherto. It charted a rapid recovery from the pandemic with a reduced level of long-term damage. The country is indeed rapidly recovering from the shutdowns that disrupted the economy, making the furlough scheme in particular redundant, and this does improve the economic statistics – but beyond that this all chaff. The tax rises have little to do with the social care crisis; rising prices mean that the Universal Credit cut is causing hardship; economic forecasts have a paradoxically backward looking methodology which makes them very unreliable. Mr Sunak has navigated these treacherous waters cleverly, but what does this all mean in the cold light of day?