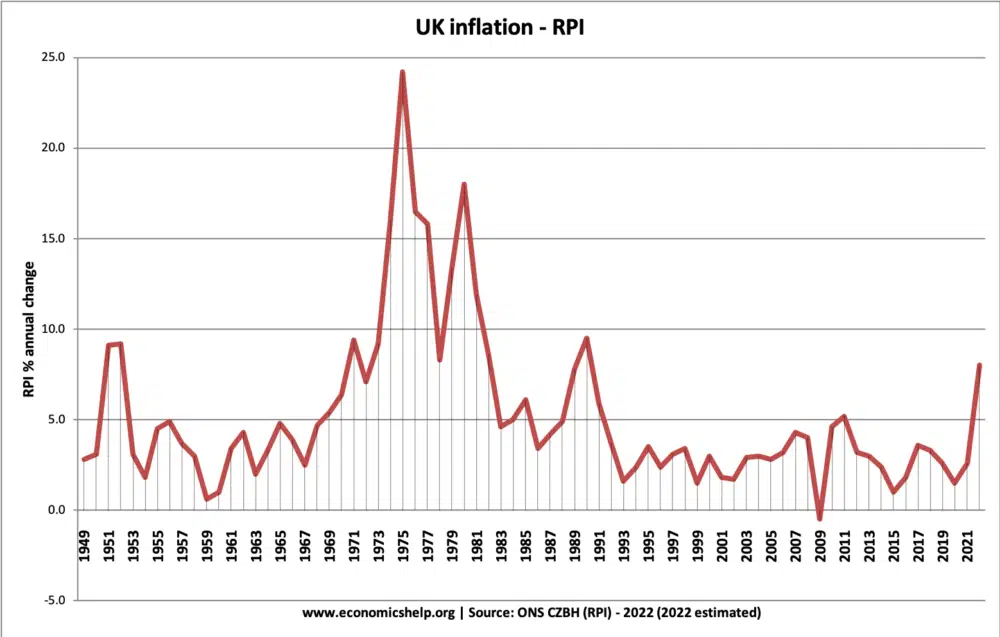

I remember Britain’s inflation crisis of the 1970s well. I was a teenager, just coming into political consciousness. I started subscribing to The Economist newspaper in mid 1974, between the two British general elections in that year. Back then I was a firm supporter of the Conservative Party, which then entailed being a Europhile. Disillusionment did not overcome me until the end of the decade. Inflation remained the dominant economic issue until well into the 1980s. But these days most people in political power, political or economic journalism, or with economic responsibility are from a younger generation, who have only read about those times. I don’t think they have quite understood what is happening.

A number of things jar. The first is that discussion often fails to take in the difference between real and nominal statistics. Nominal data is simply the raw figures expressed in currency. These become of limited use when inflation takes hold, if you wanted to compare prices and values over time. So the concept of “real” data, adjusted for inflation, was developed. GDP data is expressed this way now as standard – as is almost all material in standard economics courses. Still, there has been a fashion of advocating monetary authorities targeting nominal GDP, rather than inflation. The concern was that if both real growth and inflation were very low, then the economy should be stimulated, even though inflation might not appear to be a problem. For a developed country, I think, the suggestion was that the target should be in the region of 5% per annum – allowing for 2-3% inflation alongside a “normal” rate of growth of about the same rate. It is now running at about 12% in the UK, showing an extreme overshoot. That suggests a case for hard monetary tightening – though, to be fair, with inflation at 9% and projected to go higher, an inflation-only target does the same job.

And that, if you read most comment, is exactly what the Bank of England is doing now, with a 0.5% rate rise recently, the highest increase since it became independent in 1997, we are told. But the “real” concept applies to interest rates too. The real rate base rate, by my calculation is around minus 7%. I find myself asking how can that can be described as tight. More seriously, it suggests that cash savings are being eaten away at a rate of knots. Other investments, apart from residential property, don’t look a much better bet either. Wealth is being destroyed at a rate we haven’t seen since the Great Financial Crisis – though conservative investors would have done well out of that episode in a way that they are unlikely to today (unless they held substantial amounts of index-linked stocks). Of course, it is not hard to see why people seem so unconcerned. The political weight of borrowers, and especially those with mortgages on their homes, has always been greater than that of savers. And higher nominal rates imply more cash flow stress on mortgagees, when income may not be guaranteed to keep pace. Still, I find it a bit jarring that there is so little political pressure to raise interest rates. A backlash from savers may yet emerge.

A further jarring side to the current discussion is that so many seem to think that inflation and growth are variables that are more or less independent of each other. An extreme example comes from Liz Truss’s campaign for the Conservative leadership. She seems to think that policies to support growth, or stop a recession, are independent of policies to curb inflation. she was a bit shocked when Chairman of the Bank of England suggested that attacking inflation would affect growth. At the same time, one her supporters, Suella Braverman, suggested that the Bank is to blame for inflation getting out of hand, and should have raised rates earlier – apparently impervious to the idea that this would have dented the growth that ms truss seems to hold as a sacrosanct economic objective. But growth and inflation are two sides of the same coin. You can’t stop inflation without putting pressure on demand, which limits growth. That’s politics, I suppose, but such comments should be enough for Ms Truss, and especially Ms Braverman, to be laughed out of court. If you you are in favour of tackling inflation, you should accept the risk to growth, and even welcome it. If you think inflation will disappear of its own accord (because it comes from external sources such as oil prices), then you should say so outright. But if you do, you face a tricky question on pay. If pay does not keep up with inflation, then real incomes will shrink – which means recession. So, if you want to avoid that, you should be more supportive of public sector pay increases. No senior Tory is in favour of that. In fact a growing part of inflation now seems to come from a wage-price spiral. This is exactly what you would expect when unemployment is as low as it is, and many employers face problems with recruitment, not least in the public sector. That means that any policies that support growth will make inflation worse.

Still, this is not the 1970s. Then the main industries were heavily unionised, and the public sector was huge, including public utilities, the coal and steel industries and a big car manufacturer. The size of payrises were front and centre of economic management and political discourse; strikes were commonplace, and not subject to the heavy regulation of today. It was much easier for inflation to become entrenched. It was also hard for major businesses, and especially the public sector, to push through productivity-improving changes to working practices. Stagflation was the result. Today, inflation should be much easier to bring under control.

Today’s discourse on inflation is right about one thing: one of the critical issues is hardship inflicted on the less well off. Funnily enough, I don’t remember people talking about this in the 1970s. Perhaps there was less financial insecurity, and benefits were relatively more generous – that is certainly a popular narrative on the left, but I would like to see more evidence before accepting that to be the case. It may just be my tilted memory. It is certainly one of the biggest talking points now, though it is hard to know just how widespread the hardship is. There is certainly plenty of it, as we can see even here in leafy East Sussex.

What is clear to me is that a recession of some sort is required to bring the economy under control. That means a reduction in overall living standards – and public policy should ensure that this burden mainly falls on those on middle and upper incomes. And that points to higher taxes and more “handouts” – at least in the short term. Alas our probably next prime minister is saying the opposite.

“I don’t think (the younger generation) have quite understood what is happening.”

Neither have most others.

The problem lies in the interpretation of the word ‘inflation’. It is generally, in econo-speak, split into the two types of demand-pull and cost push. Supply push is probably a better term. It is generally accepted that our present woes are caused by a lack of supply caused by a combination of Covid, war, climate change induced natural disasters and an effective international energy cartel. Yet the applied solution is based on what we might or should do if it were a primarily a demand-pull induced inflation.

There is some of this. It has been caused by the loose fiscal policies that were necessary to maintain a functioning economy during the Covid crisis, so the reality doesn’t fit neatly into the accepted theory. We have both demand pull and supply push inflation factors at work simultaneously.

Nevertheless the mainstream is wedded to the notion that somehow a partially fiscally induced problem has a totally monetary solution. This makes little sense and is a recipe for another 2008 style financial disaster.

I’m really not sure there is any remedy at all for the supply side component. If there is less oil and gas available then prices will have to rise as a rationing mechanism. Deliberately creating a recession won’t give us a bigger ration! This will mean having to still pay the higher bills out of a reduced income. Those who lose their jobs won’t agree that anything has been brought under control. If it all gets as bad as I think it might, we’ll have created ideal conditions for an uncontrollable new fascism to emerge.

As I see it inflation is a manifestation of excess demand, whether that is the result of a demand shock or supply shock. So the solution is (usually) to reduce demand to the new equilibrium level. This could be achieved by everybody taking a real-terms pay cut, with no other change. We would then adjust our consumption accordingly, spread out over the whole economy. There is unlikely to be much unemployment as a result (well, that may be a bit starry-eyed), but it would still amount to a recession. Of course if you could simply quickly increase supply in the right goods (i.e. those that match where the supply shock was – or substitute), then that would be the best of all. But that doesn’t happen very often. And not an option now!

Interest rates are a very imperfect instrument through which to manage demand, though, which is why the old neoKeynesian economic consensus was flawed. Fiscal policy is capable of a much more refined approach. I agree with you on that!

@ Matthew,

Your last comment means that the crisis has to be paid for entirely by reductions in workers’ pay but those who have accumulated savings will be protected.

It’s not going to happen this way, whatever either of us might think. I would say to keep nominal pay constant and share out the cost equally as far as possible. Even this will be politically difficult. There will inevitably be a class conflict. The labour movement will naturally do what it can to keep its members living standards from falling.

Probably MPs won’t help by using the recent inflation figures to justify their own pay rise.

Yes I was looking at an idealised world with thought of what might cause the least dislocation – including the protection of savings. It isn’t necessarily the fairest way forward – but it does illustrate that you can have a recession without job losses, in theory. Reducing previously accumulated savings is a much less sure way towards reducing consumption in the short term. But as you say, unions will push to protect their members’ living standards. And where the labour market gives them leverage – which is a lot of the time these days – they will succeed. Some creative disruption ensues. Good capitalists shouldn’t have an issue with that – but it does point to the need for fiscal restraint.

“… you can have a recession without job losses, in theory. “

Yes this is an interesting observation. If there was a supply shock of, say, 5% then we’d agree to take a 5% pay cut. We’d all keep our jobs, demand would match up with supply and there be no increase in inflation.

Alas in the real world……..